The past few years have been challenging for the Indian port sector. A weak global environment coupled with tardy project execution, subdued investor interest, cancellation of contracts, and lack of clarity on the policy front has hampered sector progress. For the past five years (2010-11 to 2014-15), traffic at Indian ports witnessed single-digit year-on-year growth. In 2015-16 (till September 2015), cargo traffic at Indian ports grew by only 1.9 per cent, compared to 7.2 per cent in 2014-15.

To improve sector performance and drive growth, the government has become proactive and is undertaking various steps to address long-pending issues. The Rs 4,000 billion investment envisaged under the Sagarmala programme is expected to increase port capacity and improve operational efficiencies. Given the policy and fiscal push that coastal shipping has received in the past year, overall coastal traffic at ports is likely to pick up pace. Further, the cabotage relaxation could result in increased container movement.

To a great extent, activity in this sector will always be correlated with global economic growth and international seaborne trade. However, there is a need to address the long-standing issues and concerns as well as build capacity. The key lies in giving top priority to resolving issues impeding effective and timely execution of projects.

Size and growth

- India’s 7,517 km coastline is dotted with 12 major and about 200 non-major ports.

- During the five-year period 2010-11 to 2014-15, cargo traffic at Indian ports grew at a compound annual growth rate (CAGR) of 4.4 per cent, increasing from 885 million tonnes (mt) to 1,052 mt in 2014-15. For the first time, the port sector crossed the 1 billion tonne mark in traffic handled. Growth was primarily led by non-major ports, which grew at a CAGR of 10 per cent during this period, while major ports grew at only 0.49 per cent.

- Major ports handled 606.37 mt of cargo traffic in 2015-16, a year-on-year growth of 4.3 per cent. Coal, petroleum-oil-lubricants (POL) and containers registered an increase of 10.3 per cent, 3.9 per cent and 3.1 per cent respectively. However, as in the previous two years (2013-14 and 2014-15), major ports fell short of the target set by the Ministry of Shipping (MoS) in 2015-16 as well. In fact, the gap between the target and actual traffic handled widened in 2015-16 to 88.75 mt, after narrowing down from 53.51 mt in 2013-14 to 23.11 mt in 2014-15.

- As per the latest estimates available for non-major ports for 2015-16 (till September 2015), traffic stood at 225.92 mt, a decline of around 1 per cent over the corresponding period of the previous fiscal. The weak performance was on account of a 28 per cent drop in iron ore volumes, an 11 per cent drop in other cargo and an 8 per cent drop in coal volumes.

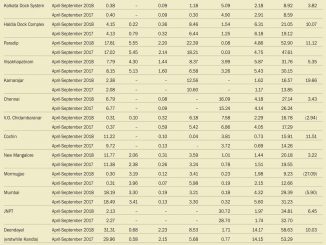

- In terms of capacity, major ports saw the highest capacity addition in 2015-16 at 94 million tonnes per annum (mtpa). As of March 2016, capacity at Indian ports stood at 965.36 mt, a capacity utilisation of 62 per cent. Port-wise, there are huge variations among major ports in terms of capacity utilisation. In 2015-16, utilisation at Mumbai port stood at 124 per cent, while at Mormugao and Cochin ports, it was 42 per cent and 44 per cent respectively.

- POL accounts for the highest share in total traffic, at both major and non-major ports. Over the years, there have been significant changes in commodity composition. Coal and containers now account for 43 per cent of the total traffic handled at non-major ports (19 per cent in 2010-11).

Key trends

- Substantial growth in traffic volumes at private ports: Adani Ports and Special Economic Zone Limited-operated Mundra port became the first commercial port in 2013-14 to handle over 100 mt of cargo in a year. Private ports, like Krishnapatnam and Gangavaram, which were commissioned as recently as 2008, have already overtaken some of the major ports in terms of traffic volumes. Some of the factors responsible for high growth at these ports are superior efficiency, diversification of cargo and deeper draught levels.

- Shift in government focus from port development to “port-led” development: The Sagarmala programme, launched in July 2015, aims to promote port-led development (direct and indirect) and provide infrastructure to transport goods to and from ports in a quick, efficient and cost-effective manner. In April 2016, the MoS launched the National Perspective Plan under Sagarmala, wherein a total of 150 projects involving port modernisation, port connectivity, port-led industralisation and coastal community development have been identified. These projects entail an investment of Rs 4,000 billion. The Make in India initiative will have strong linkages with Sagarmala, as ports will become hubs for manufacturing, trading, urban living, infrastructure growth and finance.

- New areas of growth: Ports are exploring new business areas to diversify their portfolio and reduce business risks. Cruise shipping, bunkering, and roll-on, roll-off facilities have emerged as new areas of growth for the Indian port sector. Liquefied natural gas (LNG) terminals are coming up at Kamarajar, Kakinada, JSW Jaigarh, Gangavaram and Mundra ports. Ports such as Kamarajar, Mormugao and Chennai are upgrading their cruise-related infrastructure. Ports have also started leasing their land for construction of storage facilities, etc.

- Greater focus on modernisation: Information technology solutions are being adopted at ports to enhance transparency and increase efficiency in the provision of services. The MoS has identified 104 initiatives to improve efficiency at major ports. The process of appointing consultants for the transformation of five major ports is under way. The demand for new technologies is being driven by the increasing vessel size and capacity, improvements in ship design, and innovations in the methods of cargo handling. Port-based smart cities which are to come up at Kandla and Paradip in the first phase of the Smart Cities Mission will provide ample market opportunities for technology and equipment providers.

Outlook

- Overall the country’s export-import traffic is expected to grow at a moderate rate with a slight improvement in global trade projections. The effects of slower global trade growth would be commodity specific.

- Non-major ports will continue to drive traffic growth at Indian ports. In fact, they are likely to account for about half the total traffic by 2020.

- The reform process undertaken in the past couple of years is expected to increase the overall growth of the sector. These measures include new guidelines for undertaking dredging at major ports (2015), the extension of 24×7 customs clearance facility to 18 ports, customs and excise duty exemption on the use of bunker fuels, withdrawal of 13 archaic rules under the Merchant Shipping Act, 1958, etc. The government’s plan to amend the model concession agreement for better risk allocation between the parties concerned is another welcome step.

- The Sagarmala programme will have a positive long-term effect on the port sector, in terms of improving connectivity and promoting mechanisation and modernisation. However, central and state coordination for the project will be a key factor in determining its success.

- There exists a huge pipeline of projects, both at major and non-major ports. According to India Infrastructure Research, there is a strong pipeline of projects worth Rs 900 billion in the sector, which translate into significant opportunity for developers, contractors, and equipment and technology providers. There will also be opportunities in the dredging and inland waterways segments.

- However, the reform measures are yet to translate into much action on the ground. While environmental clearances are being granted faster, several other structural constraints such as land acquisition, approvals, limited avenues for long-term funding, etc., continue to slow down project execution. Projects at major ports are being cancelled or restructured, and bid submission deadlines are being extended several times due to poor response. Major ports need to overhaul their functioning and organisation structure to prevent the diversion of traffic to non-major ports.

- Moreover, the development of new non-major ports is progressing at a very slow pace due to delays in obtaining clearances, land acquisition, etc.

- Given the tough global environment and sector-specific issues, recovery in the sector is expected to be gradual.