Once seen as the poster boy of the country’s growth, the Indian telecom sector is today on the brink of a severe financial crisis. The industry’s debt has reached a staggering Rs 4.6 trillion, revenues are on a downward spiral, profitability has taken a serious beating and operators’ liquidity position is very fragile. Clearly, the Indian telecom industry is on its weakest financial wicket since 1999, when the fledgling sector was on the verge of a collapse with several companies that had won licences under the National Telecom Policy, 1994, struggling to pay their licence fee. The government had then come to their rescue by offering a bailout package, which allowed li-censed operators to migrate from a fixed licence fee regime to a revenue-sharing scheme under the New Telecom Policy, 1999.

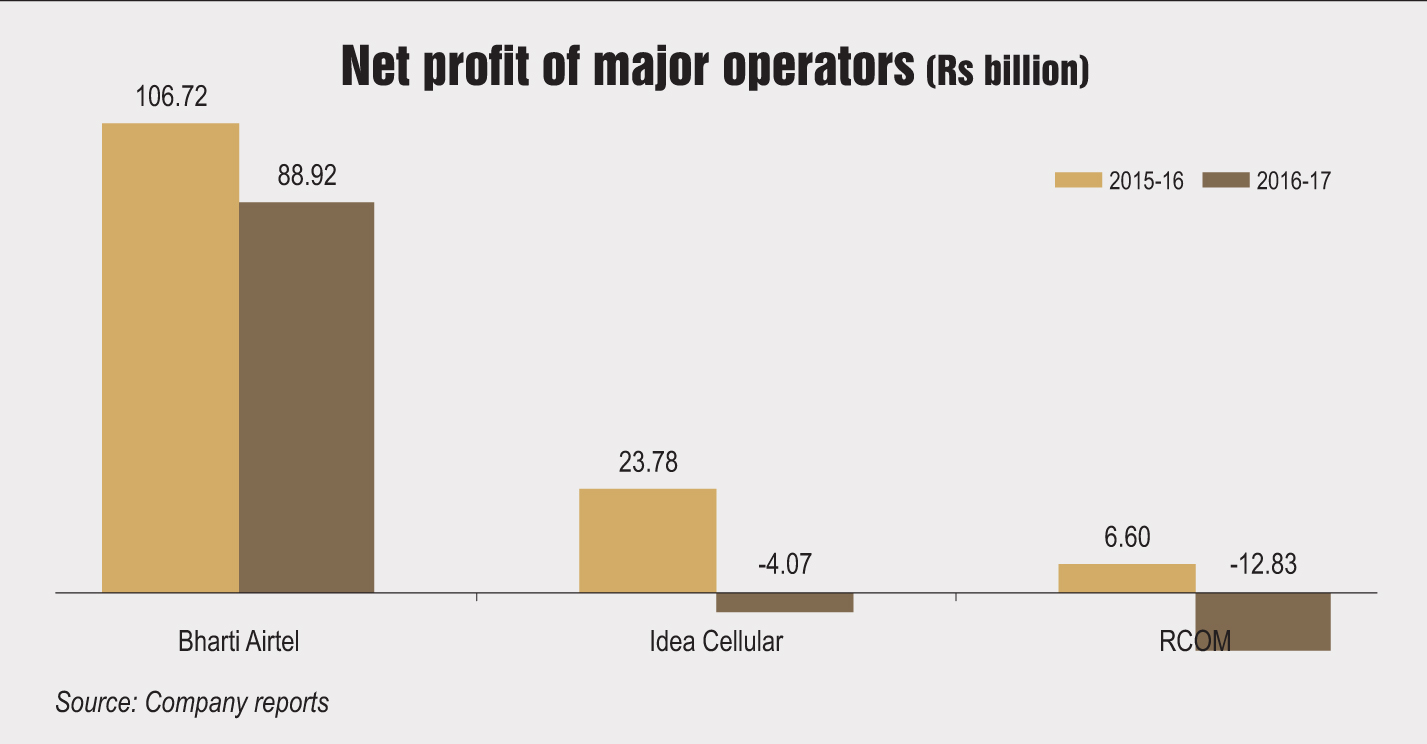

Almost two decades and a billion subscriber additions later, sinking bottom lines have returned to haunt the telecom industry. The latest earnings season indicates that the operators’ concerns are not unfounded. According to brokerage and investment firm CLSA, during the year ended March 2017, total operator revenues declined for the first time since 2008-09. Revenues slumped by 2.6 per cent from Rs 1.93 trillion in 2015-16 to Rs 1.88 trillion in 2016-17. The country’s largest service provider, Bharti Airtel, reported its lowest quarterly profit in four years as earnings plunged 72 per cent from Rs 13.19 billion during the quarter ended March 2016 to Rs 3.73 billion during the quarter ended March 2017. Vodafone India reported its lowest-ever average revenue per user of Rs 140 in the January-March 2017 period. Idea Cellular posted a second straight quarter loss of Rs 3.72 billion during this quarter.

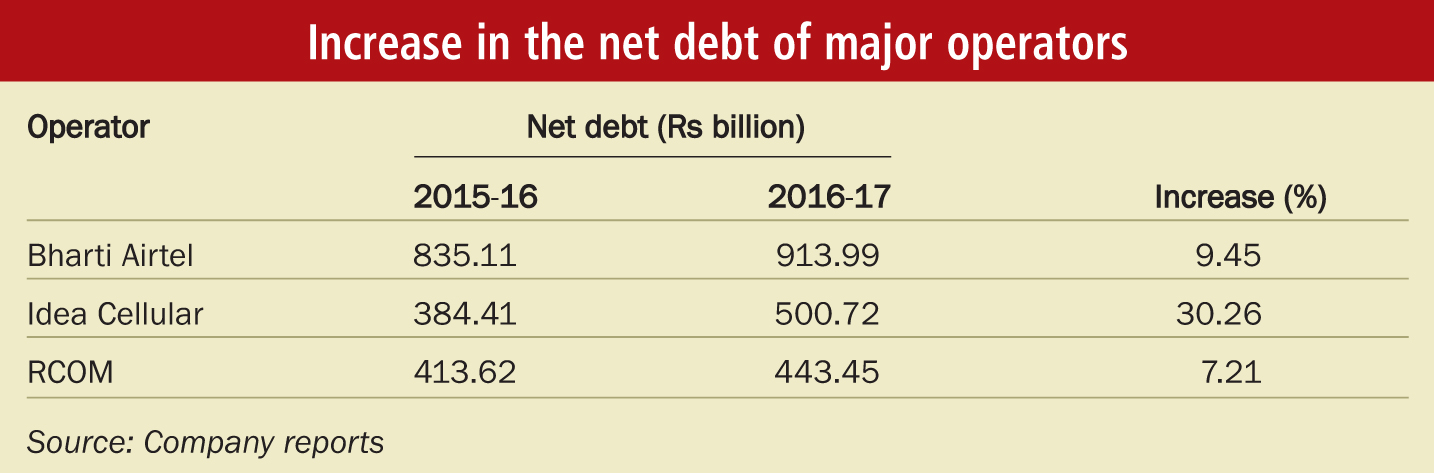

Reliance Communications (RCOM) is perhaps the worst hit. The operator reported a net loss of Rs 12.83 billion during 2016-17 against a net profit of Rs 6.6 billion in the preceding year. Its net debt stood at around Rs 450 billion, one of the highest in the industry. As investors grew jittery about the company’s debt repayment ability, RCOM’s shares dived sharply. The downgrading of the company’s debt instruments by various rating agencies on account of its weak operating performance and high leverage further deepened the investors’ worry lines.

Crisis in the making

Most incumbent operators and industry analysts have attributed the financial turmoil in the sector to the entry of Reliance Jio Infocomm Limited (RJIL) and its disruptive free service offers. The incumbents were left with no choice but to join the aggressive price war in order to defend their market shares. While subscribers benefited from the cheaper data and voice packs, these had a serious negative impact on the operators’ earnings and profitability. According to RCOM’s investor presentation, the voice revenue per minute for the industry has seen a 25 per cent decline in the last two quarters, while data revenue per MB has fallen by 40 per cent. The situation is likely to remain unchanged in the near term as RJIL, even after shifting to a paid service model from April 1, 2017, continues to be extremely aggressive in its pricing, offering data services at rock-bottom prices and voice calls still being free.

While RJIL’s entry has undoubtedly increased the intensity of competition in the industry, it can only be held partly responsible for the industry’s dismal financial condition. The sector has been under pressure for the past eight years, much before the beginning of “the free service era”, on account of increasing capex intensity. The capex incurred by operators has grown substantially and continuously on account of a rising tax burden and high spectrum acquisition costs.

Telecom is one of the highest taxed sectors in the country. The cumulative tax incidence of the telecom sector in India adds up to about 33 per cent of revenue as compared to 20 per cent in the European Union, 22 per cent in China and 17 per cent in the US. According to the Union Budget 2017-18, telecom companies paid Rs 780 billion to the Department of Telecommunications (DoT) in 2016-17 by way of recurring licence fees and other charges. The gross liability of the telecom industry on account of debt as well as payments related to spectrum amounted to Rs 7.75 trillion as on March 31, 2017. In 2017-18, operators will have to pay Rs 530 billion as interest and Rs 280 billion for spectrum already bought.

Adding to the industry’s woes, the Goods and Services Tax [GST] Council has decided to impose an 18 per cent tax on telecom services. At present, telecom services attract a service tax of 14 per cent, along with a Swachh Bharat cess of 0.5 per cent and another 0.5 per cent Krishi Kalyan cess. Under the new GST regime, the full input tax credit (ITC) on inputs can be availed of by telecom service providers. According to the finance ministry, this additional ITC would be as much as 2 per cent of the turnover of the telecom industry. Further, operators can avail of ITC on the service tax paid to acquire spectrum over a period of three years. All these, as per the government, would reduce telecom companies’ liability to pay GST through cash to about 87 per cent of what they paid in the previous financial year.

Telecom operators, however, contend that the increase in the GST rate for telecom services from 15 per cent to 18 per cent would be far more than the effective increase in tax credit. According to the Cellular Operators Association of India (COAI), while the increased burden of 3 per cent will impact the entire revenue, the benefit of input tax will accrue only on the procurement of capital equipment, which is a small percentage of the revenue. The COAI has further highlighted that a number of key industry inputs such as diesel and electricity continue to be outside the purview of GST. The industry has also opposed the denial of credit on telecom towers, despite the fact that towers are essential for rendering telecom services.

Banks become jittery

The financial crisis has raised concerns about the operators being able to meet their loan commitments. The Reserve Bank of India, in April 2017, asked banks to review their exposure to the telecom sector and make higher provisions to safeguard their business from future stress. In a more recent instance, the State Bank of India (SBI) requested DoT to work on a bailout package for telecom operators. As per SBI, the sector’s total earnings before interest, taxes, depreciation and amortisation stand at Rs 650 billion on an annualised basis, which is unsustainable for a debt of more than Rs 4 trillion.

Industry seeks urgent relief measures

The COAI points out that there is an urgent need to rationalise regulatory costs to prevent the financial health of the industry from deteriorating further. Its recommendations include a reduction in the spectrum usage charge (SUC) and licence fee, a five-year moratorium on deferred spectrum payments and a 12 per cent GST rate for telecom services. However, not all operators are in favour of a financial bailout. According to RJIL, telecom operators should invest more in equity than in debt in order to have sustainable operations. The company claims it has been funded by six times as much equity as debt. In contrast, Bharti Airtel has raised 33 times more debt than equity since 2010.

Government bailout

With banks joining the operators’ chorus for a bailout package, the government has formed an inter-ministerial group (IMG) comprising officials of the telecom and finance ministries to look into the matter. The group has been entrusted with the task of examining the systemic issues of viability and repayment capacity, and submitting recommendations for the resolution of stressed assets issue in the sector at the earliest.

To this end, the IMG has met several telecom firms and asked them to provide the figures for their annual revenue, operational expenses, net profit, market share, return on investments, return on capital deployed, debt liability from both domestic and foreign lenders, spectrum liability and equity infusion, among other parameters, for the past three financial years. Telecom minister Manoj Sinha and the Telecom Regulatory Authority of India have recently met telecom operators to take stock of the crisis.

Conclusion

Given the high degree of financial leverage and tight margins, the telecom industry may be inching towards unsustainable stress levels. As Kumar Mangalam Birla noted in Idea Cellular’s annual report for 2016-17, the past few years have been a period of telecom discontinuity, permanently changing the mobility business parameters. The industry has massive challenges, which, if not addressed quickly, could lead to a financial collapse in the sector.

While the industry has resorted to consolidation as a self-correcting measure, government intervention to improve industry profitability cannot be ruled out. That said, the merits of a financial bailout package in this regard are debatable. The government is finding itself in a catch-22 situation, wherein offering a bail-out deal may raise similar demands from other leveraged sectors and its absence may lead to a pile-up of bad debt.

Given the criticality of the telecom sector and the role it is envisaged to play in making the Digital India initiative a reality, it would be interesting to see if and how the government rescues the sector from a financial catastrophe.