The global liquefied natural gas (LNG) market has witnessed several key developments over the past few years, such as falling gas prices, rising LNG production and enhanced export capacities. Such developments have also impacted the domestic LNG segment. The demand for gas, both domestically produced and imported, has risen significantly in the country.

Indian Infrastructure looks at some of the key developments in the Indian LNG market over the past few years…

Rising demand for LNG imports

The shortfall of supply in the domestic LNG market is largely owing to the limited gas production. Over the past few years, this supply gap has been increasingly filled by imported and regasified LNG (R-LNG). R-LNG demand has been especially acute from the domestic city gas distribution segment, with its consumption of R-LNG being in the range of 7-9 million metric standard cubic metres per day (mmscmd) during April 2016-March 2017. Meanwhile, in 2016-17, the share of imported LNG in the total LNG supply has almost doubled as compared to 2010-11, accounting for about 45 per cent of the total supply.

Declining global gas prices have been a significant growth driver for LNG import demand. Natural gas prices have been falling across all major global indices over the five-year period 2012-16. For instance, Japanese LNG prices have fallen from $16.33 per million British thermal units (mmBtu) to $6.94 per mmBtu during the period under consideration. US Henry Hub prices have also fallen to $2.46 per mmBtu, its lowest level since 1990.

India has thus emerged as a key importer of LNG in the Asia-Pacific region. The biggest source of these imports has been Qatar. However, over time, Qatar’s share in total LNG imports has recorded a decline, from a high of 96 per cent in 2005 to 62 per cent in 2016. Some of the other key countries from which India imports LNG are Nigeria, Equatorial Guinea and Australia. Even though Australian imports to the Indian economy began as recently as 2015, the country is already the fourth largest source of LNG imports, accounting for a 5 per cent share in India’s total imports.

Diversifying India’s LNG supply portfolio

With rising LNG imports, various measures have been taken to diversify the LNG source base. This has been done to ensure competitive procurement of LNG from international markets. The supply base has thus been widened substantially, to include countries such as Yemen, Algeria, Oman and the US.

However, Qatar continues to be the primary source of LNG imports. This is largely on account of a long-term supply agreement between Qatar’s LNG producer RasGas and Petronet LNG Limited (PLL), India’s largest LNG importer. In January 2016, the price of LNG bought from Qatar was renegotiated between the two companies. According to the new terms of agreement, PLL now secures LNG supplies from RasGas at nearly half the previous rates. In addition, in January 2016, PLL also signed a contract for an additional 1 million metric tonne per annum (mtpa) supply of LNG from RasGas for a period of 12 years.

Other recently signed contracts include the agreement between US-based Magnolia LNG and India’s VGS Group for the supply of 4 mtpa of LNG. It will be sourced from the Magnolia terminal in the US for the Krishna-Godavari floating terminal in India, for a period of 20 years (2022-42). Meanwhile, GAIL (India) Limited has signed a time-swap deal with Swiss trader Gunvor for 15 cargoes (about 0.8 million tonnes) of LNG during April-December 2017.

GAIL has also set up an overseas investment arm – GAIL Global (Singapore) Private Limited – to source spot cargoes for the Indian market, and for trading in LNG, petrochemicals and related products. At the same time, several companies are also aggressively investing in overseas gas reserves. For instance, ONGC Videsh Limited, Oil India Limited and Bharat Petroleum Corporation Limited together hold a 30 per cent stake in six blocks in the deepwater Rovuma basin, off the Mozambique coast in southern Africa.

Further, companies such as PLL, GAIL, Gujarat State Petroleum Corporation (GSPC), ONGC and Oil India Limited have signed long-term contracts with several LNG suppliers including Australia, Russia, the US and Mozambique. However, these projects are scheduled to begin only after 2018-19.

Expanding terminal infrastructure

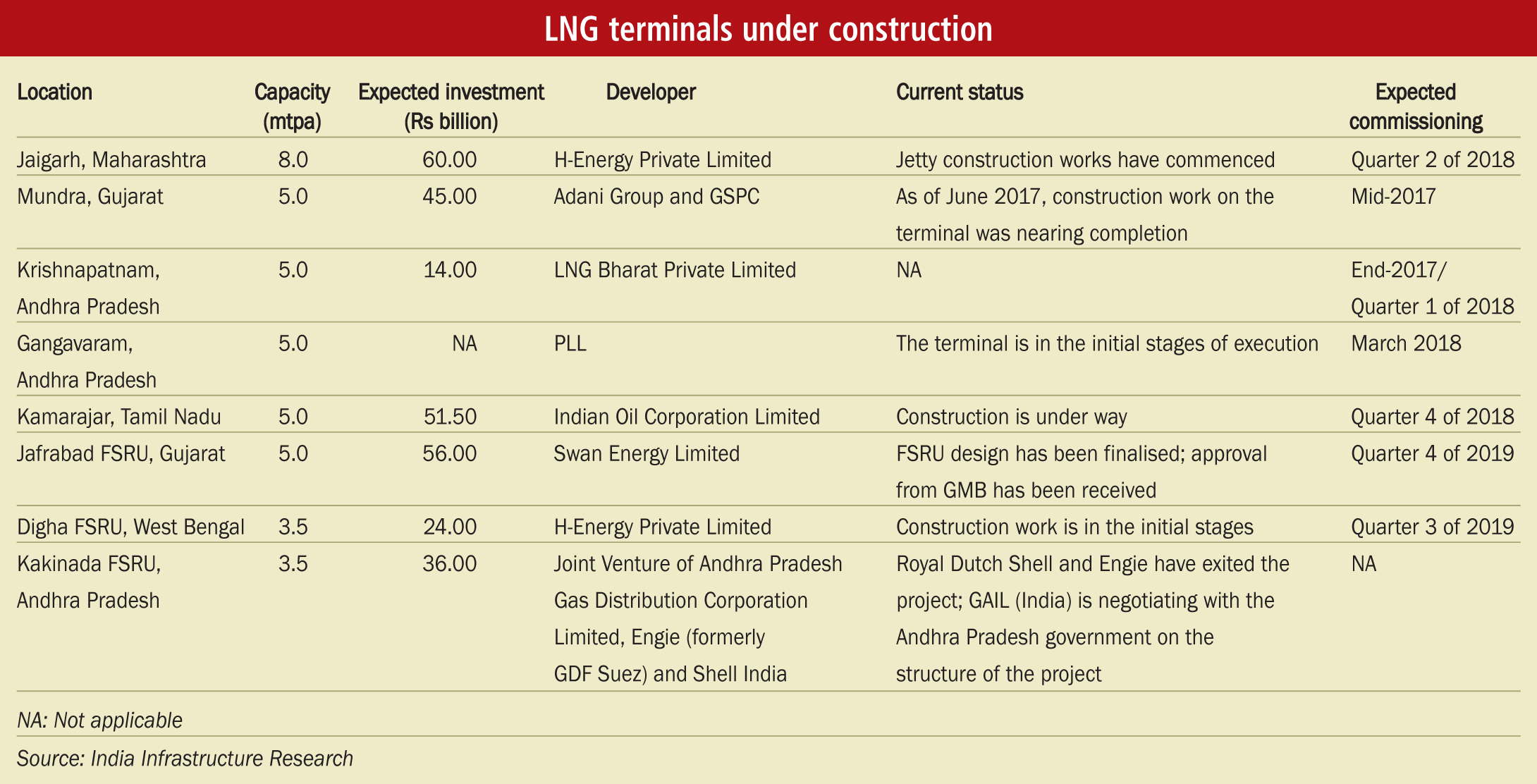

At present, there are four operational LNG import terminals in the country. Together, these terminals have an aggregate regasification capacity of about 27 mtpa. In the coming years, the capacity of these terminals is set to be expanded significantly. As of June 2017, 15 key LNG terminals with an aggregate capacity of more than 73 mtpa were either under implementation or had been proposed/announced to be taken up in the future. These upcoming LNG terminals are expected to entail a total investment of at least Rs 490 billion.

Of this amount, about 58 per cent of the funds (Rs 286.5 billion) will be spent on projects which are currently under implementation. Presently, eight LNG terminals with a combined capacity of 40 mtpa are being developed across the country. The largest capacity will be developed at Jaigarh in Maharashtra (8 mtpa). Most of these terminals are expected to be commissioned by 2018-19.

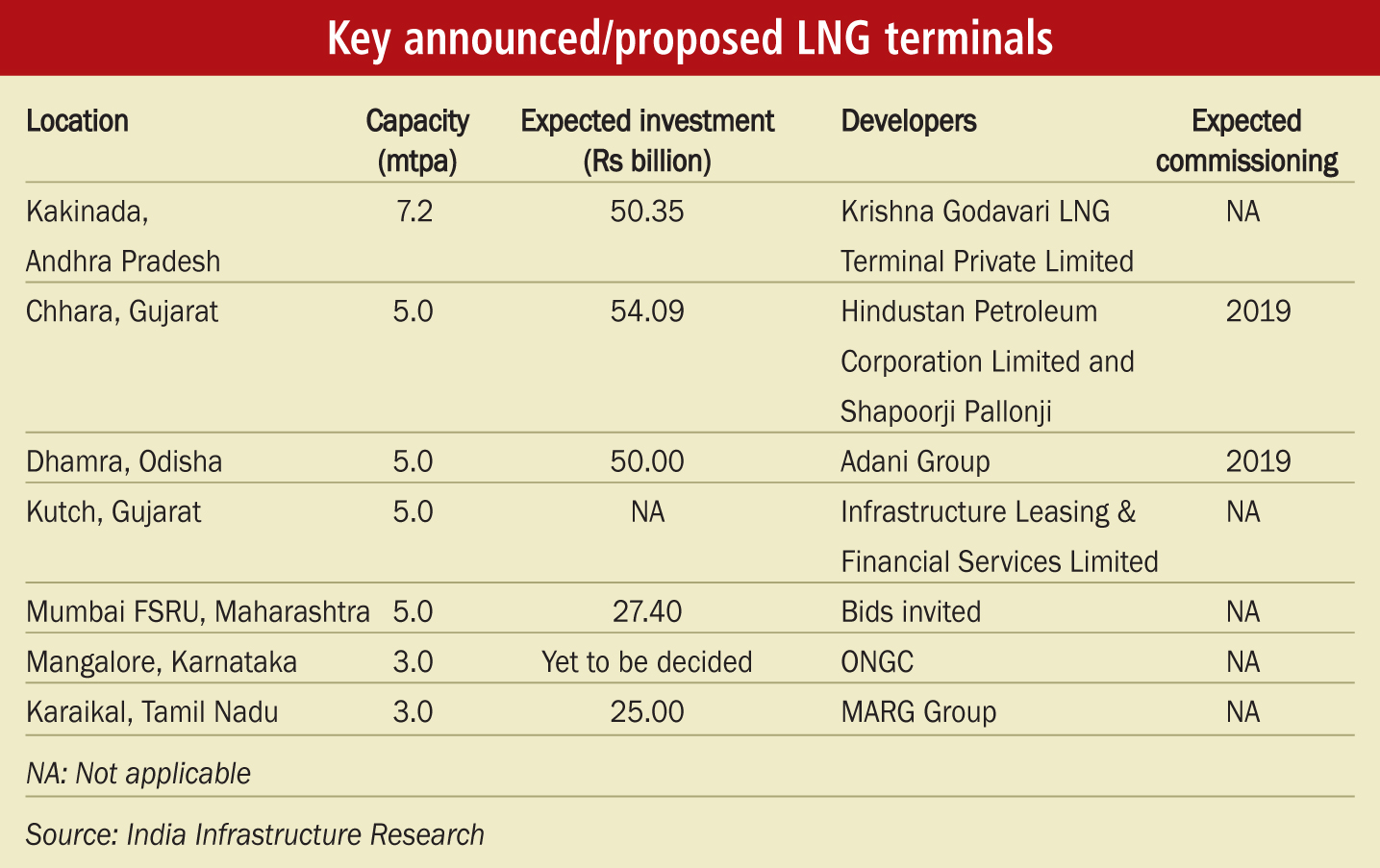

Meanwhile, investments of Rs 206.84

billion are being envisioned for announced/proposed LNG terminal projects. India Infrastructure Research has identified seven such key terminal projects, which will have a total combined capacity of about 33 mtpa. Of these, about 51 per cent (37.2 mtpa) of the proposed capacity will be constructed along the east coast. The largest facility, the Kakinada terminal in Andhra Pradesh, will have a capacity of 7.2 mtpa.

The way forward

As per industry estimates, the global LNG export capacity is expected to increase by at least 500 mtpa between 2015 and 2021. However, this rise in global LNG production and export capacity will be subject to declining gas demand in regions such as Europe, Japan and Korea. At the same time, LNG will face stiff competition from the rising renewables and coal-based energy generation.

In sharp contrast, gas demand in the country is set to grow significantly in the short to medium term. According to ICRA, domestic gas demand is projected to increase from 234 mmscmd in 2016-17 to 286 mmscmd in 2024-25. At the same time, supply has been forecasted to grow from 107 mmscmd to 185 mmscmd during the same period. However, this projected growth in supply will still not be able to keep up with domestic demand requirements. Thus, while the forecasted demand-supply gap is set to reduce from 127 mmscmd to 101 mmscmd during 2016-25, a significant proportion (about 35 per cent) of the future demand will still not be met by domestically produced gas.

Therefore, to meet its domestic gas requirements, the country is expected to increase LNG imports in the future. Further, in line with its supply portfolio diversification plans, the government has also announced its intention of importing LNG from new source markets such as Canada and Mozambique. Therefore, India is all set to take centre stage in the global LNG market in the years to come.