")

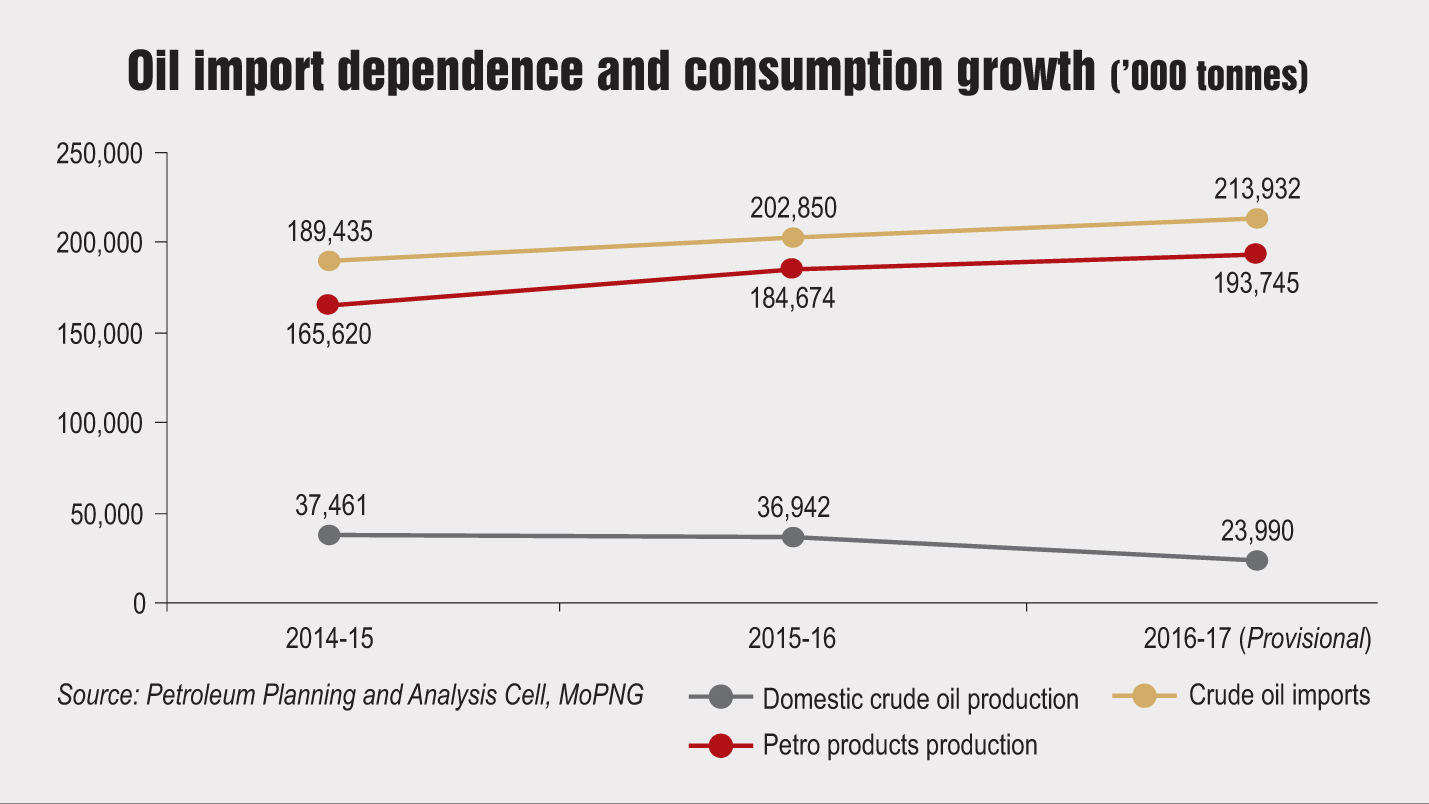

The consumption of petroleum products has grown incrementally in India with domestic production failing to keep pace with demand. This has led to a massive spike in imports.

Taking cognisance of the very high import dependence, the government announced (in 2015) that it would like to bring oil and gas imports down to 67 per cent by 2022. In 2016-17, import dependence stood at 82 per cent.

During the past 12-18 months, the Ministry of Petroleum and Natural Gas (MoPNG) has introduced a number of policies and reforms aimed at increasing domestic output. Approved by the government in September 2015, the Discovered Small Fields [DSFs] Policy, 2015, was one among the slew of such policies expected to help reduce the country’s dependence on oil and gas imports. The Directorate General of Hydrocarbons (DGH) has identified 69 small fields for development (63 are of Oil and Natural Gas Corporation Limited [ONGC] and 6 of Oil India Limited [OIL]). The onshore marginal fields (33) are in Assam (12), Andhra Pradesh (8), Gujarat (5), two each in the states of Nagaland, Rajasthan and Tamil Nadu, and one each in Arunachal Pradesh and Madhya Pradesh. The offshore marginal fields (36) are located in Kutch (1) and Bombay Offshore (28) off the west coast and in the Krishna-Godavari basin (7) off the east coast .

Overall, these 69 fields are estimated to have 89 million tonnes of oil and gas resources. ONGC and OIL had not developed these fields due to various issues like remote location, small size, prohibitive development costs and technological constraints.

The first bidding round for DSFs, which was launched in May 2016 and concluded in November 2016, received an enthusiastic response from the industry. The perception of many players on DSFs has changed significantly after looking at the data available on the National Data Repository. The industry seems reasonably happy with the transparent bidding round and the significant reduction of the regulatory burden. Some of the recent developments that have had a positive impact on the industry are the provision of marketing and pricing freedom for both oil and gas, revenue sharing with the government in place of the earlier cost recovery-based production sharing, and permission to explore conventional and unconventional hydrocarbons such as shale under a single licence.

Experience of DSF Round I

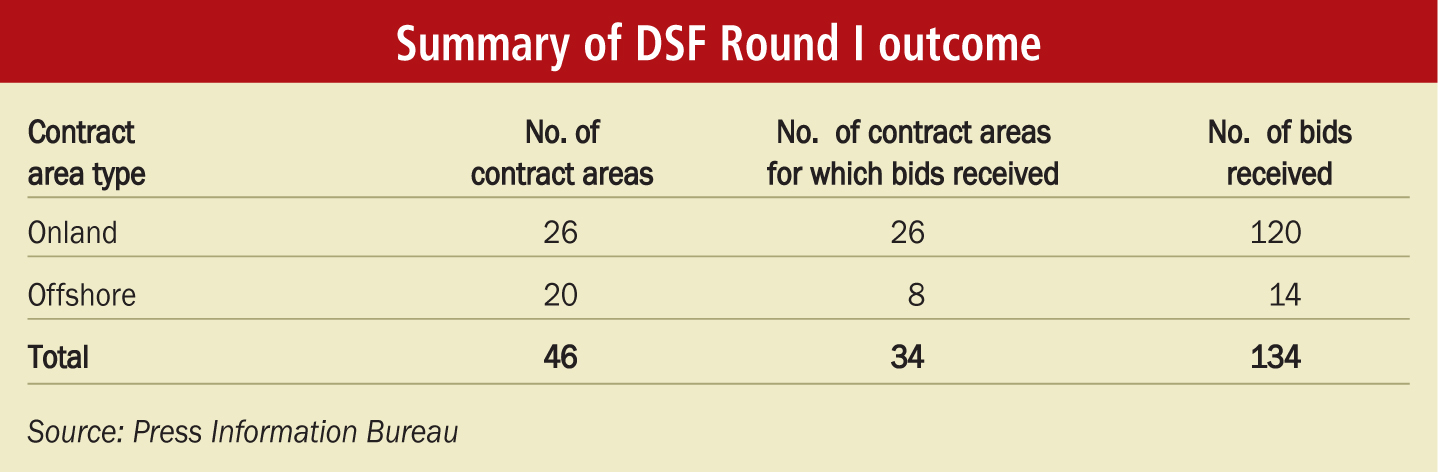

Of the 69 fields identified under the policy, 67 fields were put up for bidding under Round I. The 67 discovered small fields on offer are spread over nine sedimentary basins and offered in 46 contract areas – 26 onland, 18 in shallow waters and two in deep waters. Two fields – Chumukedema and Tynyphe – located in the Assam shelf in Nagaland were not bid out though they had been identified in the policy document.

The bid round was launched on May 25, 2016 and responses were received until November 21, 2016. The DGH received 134 e-bids for 34 contract areas from a total of 42 companies. The bid round took place in a challenging global market environment when oil and gas prices were volatile and investment in the exploration and production segment had seen a substantial decline. Despite these challenges, the response to DSF Round I has been very encouraging and exceeded expectations of experts.

Despite smaller contract areas on offer, the response from the private sector was overwhelming with several new firms successfully bidding for projects. Of the total 42 companies that participated in the bidding, five each were public sector undertakings (or their subsidiaries) and foreign private companies while the remaining 32 were domestic private companies. The evaluation of bids was conducted within two months and the Cabinet Committee on Economic Affairs (CCEA) approved the award of 31 contract areas in February 2017. Contracts for these were signed on March 27, 2017.

According to the latest information available from the DGH, contracted firms have already begun acquiring mining licences. The expected cumulative peak production from the 31 approved blocks – 23 onland and 8 offshore – is expected to be around 15,000 barrels per day of oil and 2 million metric standard cubic metres per day of gas, with a total revenue generation of about Rs 464 billion. The government’s revenue share is expected to be to the tune of Rs 93 billion. Besides, government royalties on the expected output – which is around 2 per cent of India’s current oil and gas production – are estimated at Rs 50 billion.

Other key activities to be undertaken by the selected companies include transferring the lease from OIL/ONGC to them, obtaining environmental clearance (after submission of the environmental impact assessment report) and forest clearance (if forest area is involved), constituting a management committee with members from the government as well as the operator, and preparing a field development plan (to be generally submitted within six months of the effective date of the contract) with estimated annual production numbers. The DGH will also provide the technical data to the companies.

DSF Bidding Round II

The second round of DSF bidding, scheduled to be launched in September 2017, will include the 12 offshore acreages which did not receive any bids during Round I, along with new blocks. Although so far no official communication has been made regarding the blocks expected to be auctioned in Round II, about 60 or more blocks are expected to be thrown open for bidding.

According to industry experts, for DSF Round II, potential bidders expect the government to retain the liberalised regime rules such as no prior technical experience being required, no restrictions on exploration activities during the entire contract period, a favourable pricing mechanism, and a moderate royalty structure.

“In my view, this round can be even better in terms of response, as smaller players are very eager to enter. However, it all depends on the nature of the blocks, their hydrocarbon reserves, prospects for production, and bidders’ assessment of the ease of doing business in a given geographic location,” says Ajay Kansal, deputy general manager, Production, DGH, MoPNG.

At present, the finalisation of blocks to be put on offer is ongoing.

The way forward

According to the Energy Information Administration, despite favourable policies such as the DSF and the Hydrocarbon Exploration and Licensing Policy, India’s import dependence is expected to increase to 90 per cent by 2040 on the back of high consumption growth. For import dependence to go down as targeted, the growth in domestic production will have to outstrip the growth in demand in a sustained manner.

In this regard, the government has launched a number of policy measures such as the Open Acreage Licensing Policy along with the National Data Repository that are expected to address a major drawback of the New Exploration Licensing Policy regime that forced exploration companies to bid for projects chosen by the government. Further, the government’s policy to incentivise production from ageing fields using the capital and technology intensive enhanced oil recovery (EOR) technique is expected to play a key role in attracting investments in the exploration and production segment. (EOR is a special technique used by upstream oil and gas companies to increase the amount of crude oil that can be extracted from a field.)

In addition, DSF Rounds I and II will also play a small but significant role in increasing the country’s indigenous oil and gas production. However, for the success of the DSF bidding rounds, clarity on connectivity and sharing of facilities and the method used for determining the market price of DSFs will be necessary.