")

A year ago, in September 2016, Reliance Jio Infocomm Limited entered the Indian telecom industry with an aggressive pricing strategy. It started with an offer of free data services for a period of three months but ended up extending the offer for the next six months. It also committed to permanently providing free voice calls.

Jio rapidly garnered a large subscriber base as price-conscious Indian users rushed to try out the free services. Even when the services went paid, there was a fairly good conversion rate. Jio succeeded in retaining a large proportion of the initial base as paid subscribers. It has since followed through with a new plan where it bundles a new “free” handset with a three-year lock-in plan. That concept has reportedly received an excellent response.

The consequences of these offers have been telling on the sector. Other operators responded to the price war by unveiling new offers to try and retain their respective subscriber bases. ARPUs have dropped, especially in the data segment, though India has become the largest data market in the world by volume. The financial stress is telling on the sector and forcing consolidation. Fears have been voiced by bankers and in government circles that the sector’s struggles to service debt could trigger a crisis.

Looking forward, tariffs are expected to continue falling. At the same time, subscriber growth is likely to plateau since there is already a large base. Hence, in the absence of significant new growth prospects, telecom service providers will be attempting to claw market share away from each other. In marketing terms, operators will be looking to persuade their low-end subscribers to move more heavily into data consumption since that appears to be one of the few growth channels. Operators other than Jio will also have to keep investing in maintaining their current legacy 2G networks for voice-only customers and in ramping up 4G. The response to new spectrum auctions, if any, may be subdued, since operators are already up to their gills in debt. This would impede future 5G roll-outs.

The debt trap

The Economic Survey (Volume 2) points out that Telecom Regulatory Authority of India (TRAI) data indicates that since September 2016, industry ARPUs have on aggregate come down by 32 per cent. Gross revenue for the industry declined 11 per cent, quarter on quarter, to Rs 408 billion in the quarter ended March 2017. An analysis by Credit Suisse estimates that the share of telecom debt owed by companies with interest coverage of less than 1 has more than doubled since late 2016, climbing above 55 per cent of the total long-term debt of the telecom sector.

The interest coverage ratio divides the interest outflow in a given period by the operating profits (earnings before interest, taxes, depreciation and amortisation) during the same period. If the interest coverage drops below 1, interest payouts cannot be made out of the profits from normal operations. The “vulnerable” debt held by telecom operators with interest coverage of below 1 is estimated at Rs 1.5 trillion. The Economic Survey points out that government finances are directly exposed since the industry owes it a variety of fees and taxes.

Bankers share these apprehensions. Banks have an exposure of Rs 4 trillion (the total debt exposure of the sector is Rs 7.5 trillion, which includes fees owed to the government, overseas borrowings, etc.).

Consolidation

Falling revenues and the necessity to service high debt have triggered a series of mergers. The biggest would be the Idea-Vodafone merger. This is a $23 billion transaction that will create an entity of 400 million subscribers with approximately 35 per cent market share and about 41 per cent revenue share. The merger is expected to be completed in 2018.

Post-transaction, Vodafone will eventually own 45.1 per cent stake in the merged entity, after selling a portion of its holdings to the Aditya Birla Group. The Aditya Birla Group, which is Idea’s parent company, will have 26 per cent shareholding, after paying an estimated Rs 38.74 billion to buy 4.9 per cent stake from Vodafone. The remaining 28.9 per cent will be held by other shareholders.

Bharti Airtel has bought Tikona Digital Networks Private Limited’s 4G business, including its broadband wireless access spectrum and 350 cellular sites in five telecom circles, for around Rs 16 billion. Airtel has also acquired Telenor’s India business, assuming the latter’s liabilities related to licence fees and lease obligations for telecom towers. The transaction did not involve a cash payment. That gave Airtel 44 million customers (increasing its user base to 307 million), as well as 1,800 MHz spectrum and 20,000 base stations.

Even earlier, Reliance Communications (RCOM) merged with Aircel (which was owned by Malaysia-based Maxis Communications Berhad). Following the closure of the deal, RCOM and the present shareholders of Aircel will hold 50 per cent stake each in the combined entity. It will carry a debt of Rs 280 billion, with RCOM and Aircel each contributing half that amount to the debt pool. Earlier, RCOM entered into a merger deal with Sistema Shyam TeleServices Limited (SSTL), following which Sistema, the Russian parent of SSTL, holds a 10 per cent stake in RCOM.

More consolidation can be expected. Globally, few circles can sustain more than three or four operators, and India is headed in that direction.

Data trends

Data usage expanded massively after Jio’s advent. This is in line with the understanding that telecom demand is extremely price-elastic. Jio’s offering of free data was countered by discounts from other operators. In September 2016, data usage stood at around 240 MB per user (blended average of GSM and CDMA). By March 2017, this had risen to 1,000 MB per user. There were 1,180 million wireless connections as of end-May 2017. About 400 million (34 per cent) were data subscribers. The data subscriber base grew at 28 per cent year on year during January-March 2017. Of the 400 million internet subscribers, about 258 million were broadband (3G/4G) subscribers. The remaining 35 per cent (140 million) were narrowband users, who may graduate to high speed data if it is available on low-cost devices at attractive prices. These are the customers Jio is targeting with its new bundled plan.

Revenue and market share

There is still potential for subscriber additions in rural markets, but urban markets are saturated, with teledensity at 173 per cent. Subscriber additions remain the highest in Category B circles. The overall teledensity increased to 93.9 per cent in June 2017 from 84 per cent in June 2016, but rural teledensity was only 57.7 per cent in June 2017.

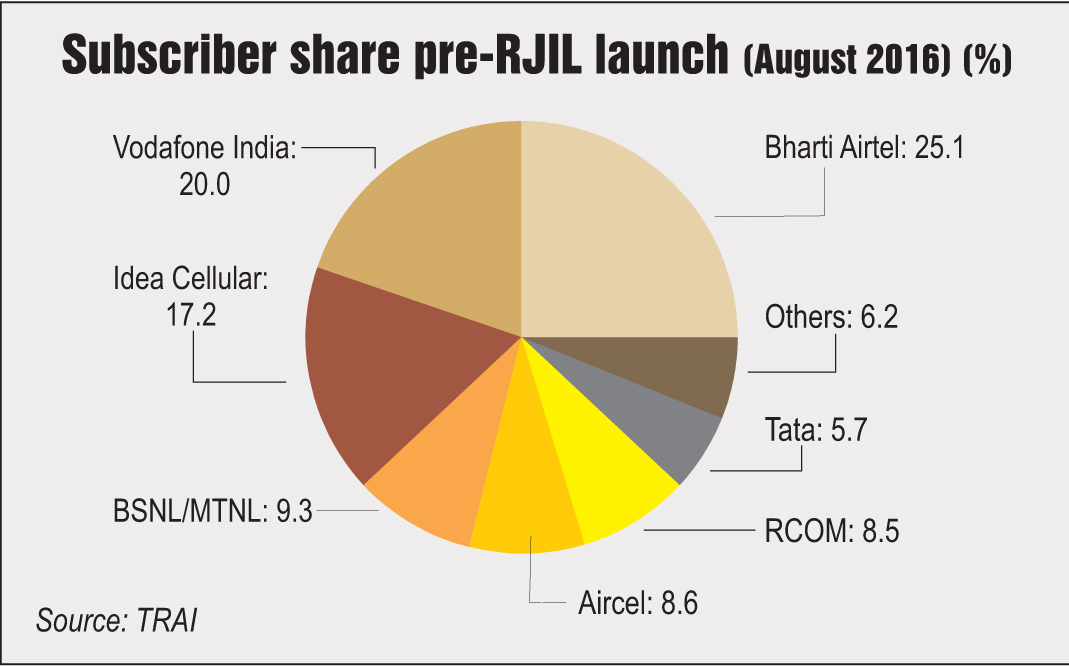

Given that the subscriber base stands at over 1.2 billion, the potential for subscriber additions is not that high. Jio gained 9.9 per cent subscriber market share between September 2016 and May 2017. It currently holds slightly over 10 per cent share with an estimated 125 million subscribers, all of whom are broadband subscribers. This gives Jio 41 per cent market share in the critical broadband segment.

Data ARPUs have fallen steeply while voice ARPUs have flattened. Data prices plunged to an average of Rs 6.40 per MB (in end-March 2017) from Rs 16 per MB (in end-December 2016). There is a possibility that the average data usage could go up again by 3x or even 4x if most 2G subscribers migrate directly to 4G.

New Jio initiative

Jio’s new initiative offers a “free” 4G internet-ready feature phone with a bundled plan. The subscriber needs to make a Rs 1,500 interest-free deposit. This is refundable after three years. The subscriber has to pay Rs 153 per month to avail of this service, with its promise of unlimited data and voice calls. The bundled phone is locked to the Jio SIM.

Analyst estimates suggest that this plan may be profitable. The cost of the handset would be more or less recovered via the higher ARPU and interest income from the deposit. Jio’s target is to persuade the “creamy layer” of 2G users to migrate; they might be tempted to pay an extra Rs 60-Rs 70 per month (and put down the deposit) to avail of the new data service. The bulk of such voice-only subscribers are rural. Hence, the competitive intensity will rise in the rural space. Jio hopes to convert some 100 million such users from pure 2G voice. What’s more, these new customers would probably be single-SIM users, unlike the current Jio subscribers who mostly use at least one more SIM. Reports say that Jio has already received over 6 million orders for the plan.

Jio finances

Jio finances

The financials of listed telecom firms show the impact. Revenues are down, margins are down. Debt service stress has increased. But Jio’s own finances are hard to assess. The business was launched only in the second half of fiscal 2016-17 and Jio did not charge for services until April 2017. Hence, making a judgement about potential revenues is difficult and likely to be error-prone. The parent, Reliance Industries Limited (RIL), had poured Rs 2 trillion worth of investments into the telecom business by March 2017. This included about Rs 1.3 trillion in debt (this includes Rs 245 billion of deferred spectrum payments and Rs 515 billion of credit from suppliers). About Rs 700 billion has been subscribed by way of equity and preference capital.

Whatever happens, RIL has the ability to sustain the telecom operations indefinitely until Jio hits break even. RIL has a huge balance sheet with a net worth of Rs 2.9 trillion and 2016-17 revenues of Rs 2.5 trillion. Other players in the telecom industry might not be able to sustain this price war indefinitely. It’s also a moot point whether other operators can compete on the basis of quality, branding and other factors.