The government’s commitment to road development has reaped substantial gains for the sector. The new models have given rise to renewed hope in the sector. Investor confidence has started to look up and road developers are seeing some scope to participate in projects. At a recent conference on “Road Development in India” organised by India Infrastructure, A.K. Singh, member, projects, National Highways Authority of India, shared his views on the progress in the road sector, the experience with new implementation models and the size and scope of several upcoming opportunities. Excerpts…

The government’s commitment to road development has reaped substantial gains for the sector. The new models have given rise to renewed hope in the sector. Investor confidence has started to look up and road developers are seeing some scope to participate in projects. At a recent conference on “Road Development in India” organised by India Infrastructure, A.K. Singh, member, projects, National Highways Authority of India, shared his views on the progress in the road sector, the experience with new implementation models and the size and scope of several upcoming opportunities. Excerpts…

Freight demand is going to increase and network planning and logistics are going to come up and make the sector more user-friendly. Previously, the sector lacked transparency, traffic estimates were not very clear and transparent, and stakeholders had to do a lot of due diligence to assess their risks. However, we have now almost moved to a platform where the entire gamut of operations which include funding, cost estimates, risks and traffic are defined transparently. Though the traffic was known, any foreign investor coming in was not very sure of the methods used and hence did not find them reliable. All the blockages that came in our way in the build-operate-transfer (BOT) model have mostly been taken care of.

Over the years, our project delivery has become much better, and we have put in place procedures to sort out all the concerns that stakeholders have. The past year saw a very large appreciation in the number of project awards, which will now drive the construction rate upwards.

Opportunities in store

We have set very ambitious targets which we hope to achieve. Through the Bharatmala programme and economic corridors, 20,000-25,000 km of road construction has been planned. The preparation of detailed project reports for projects under the Bharatmala programme is under way.

Expressways, being greenfield projects, are another area which will entail major investments. To add to the already sanctioned projects, about Rs 1.5 trillion worth of expressways have already been announced. With regard to investment opportunities, there is scope of work almost everywhere, as road development will take place in every corner of the country, some with less traffic, some with more traffic; but we will be touching the entire country and will have opportunities for local players as well.

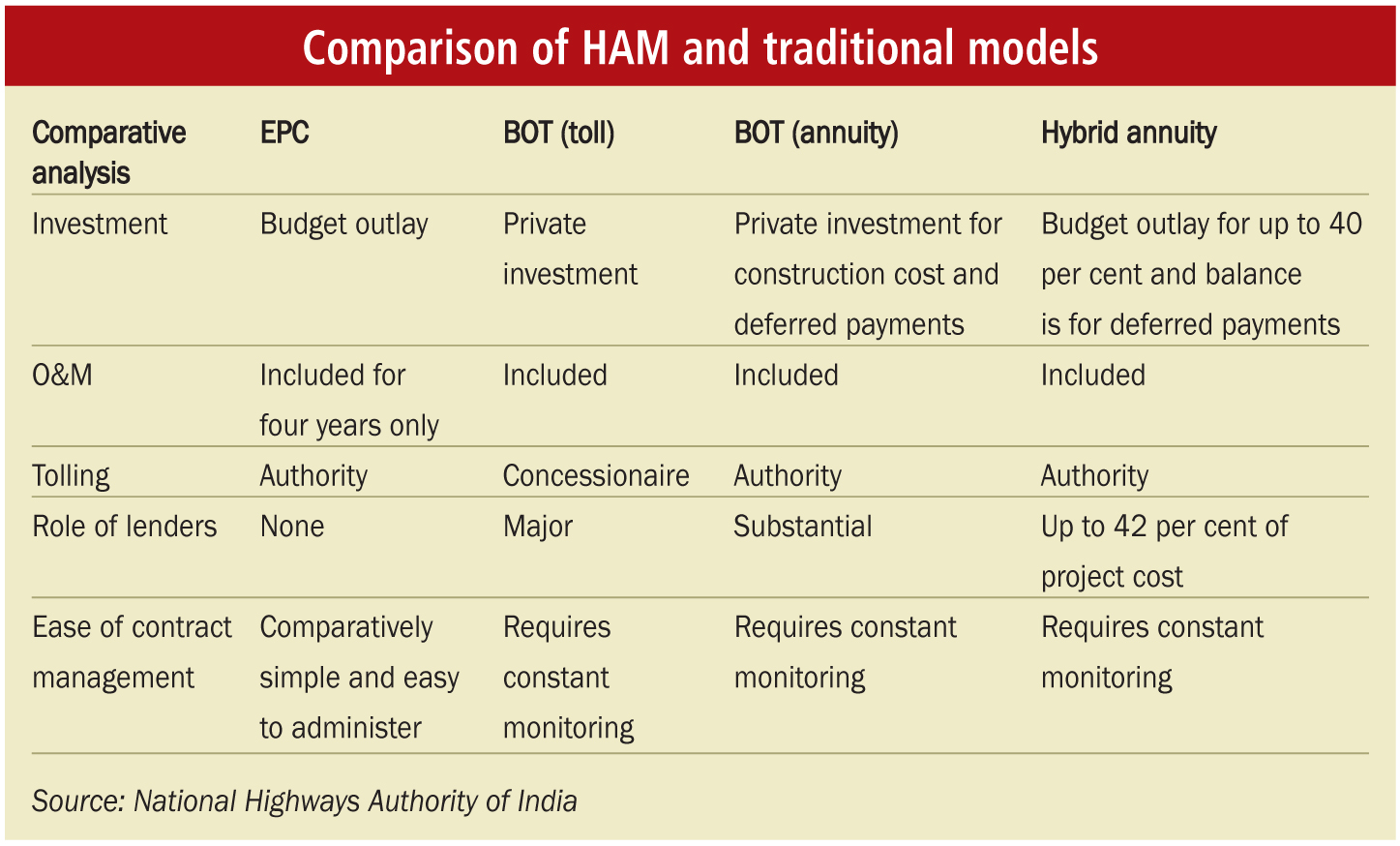

HAM and its success

The hybrid annuity model (HAM) has, to a large extent, met with success. With high-density corridors already being developed in BOT or engineering, procurement and construction (EPC) mode, hybrid annuity seemed to be the best model at this point of time. Now, 40 per cent of the project cost is supported by the government through viability gap funding and 60 per cent of the cost is arranged by the concessionaire through debt. Initially, there were hiccups because bankers who had burnt their hands due to very aggressive financing and disbursement of funds, suddenly found themselves in a tight spot. They were not very sure of this programme working out, so initially for the first six to nine months, it looked like HAM would not succeed because of bankers and lenders not supporting it, but gradually, they realised that there couldn’t be a better model – it is like an assured fixed deposit – and the internal rate of return is much more than that of government securities. We relaxed the clauses for mobilisation advances because initially the contractors were facing a liquidity crisis and they were not able to start the projects, which also sent a wrong message to the public and the lenders. Now, however, once the project is awarded the concessionaire is very eager to take up construction and even if the financing has not been arranged the construction work commences. This gives confidence to the lender fraternity. Achieving financial closure is not an issue any more for HAM-based projects.

HAM is no longer a model under testing. It has already succeeded. And now players need to be comfortable with it since the EPC model has slipped into a very competitive bidding cycle due to increased participation by contractors who are trying to increase their order books aggressively. As a result, the sector does not really have a level playing field and efficient contractors are not able to compete to get good bids.

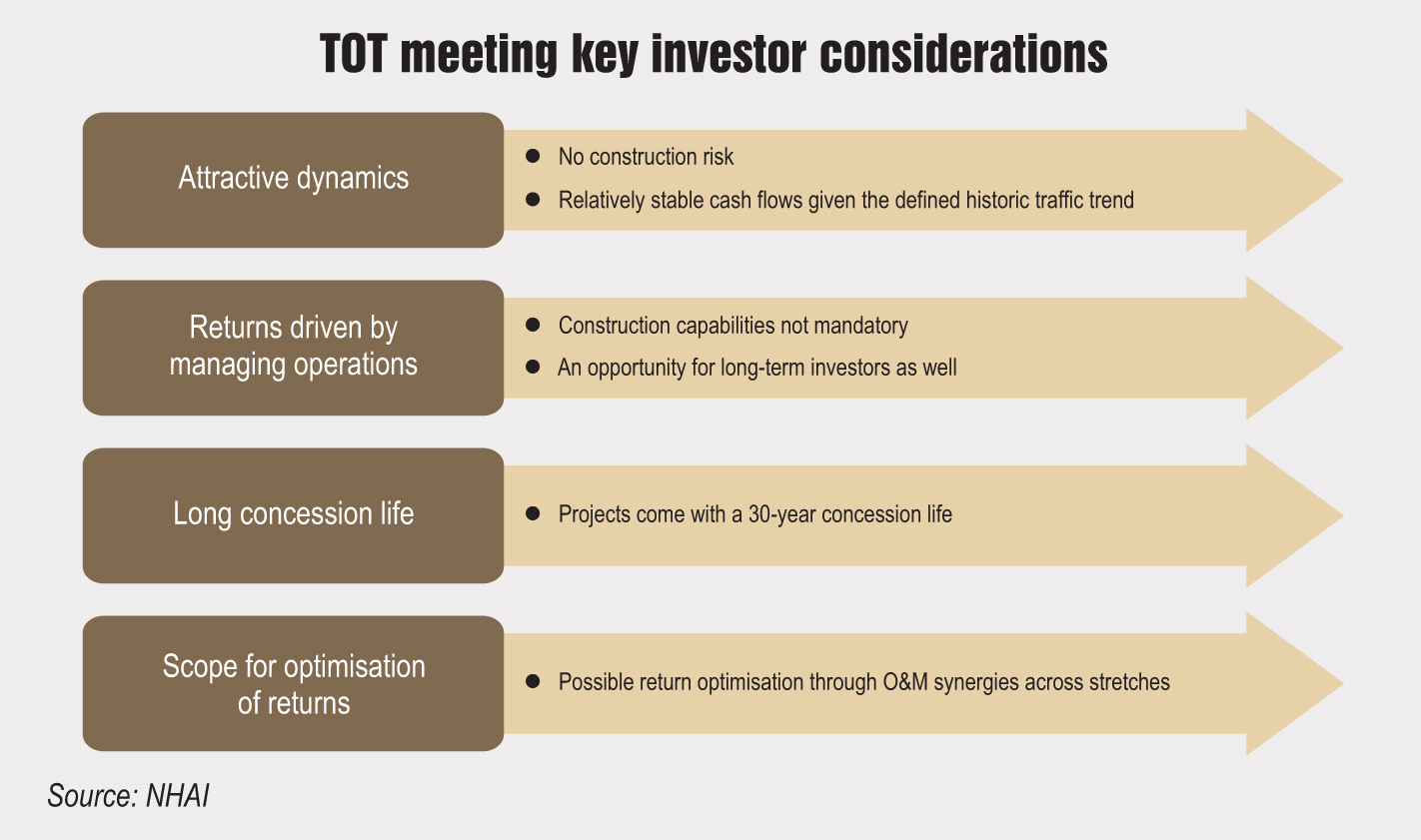

The TOT advantage

The government has been facing a lot of issues in operating and maintaining projects constructed using government funds. Since both the HAM and EPC modes have picked up, the government is in need of funds for network expansion. Toll-operate-transfer (TOT) is an upcoming opportunity where projects that were constructed using government funds will be monetised. These projects have a reliable traffic flow wherein the investors can assess the toll collections accurately, to estimate revenues and place bids accordingly.

TOT will enable the inflow of long-term funds into the sector. The investors will own the project and operate it. The concept of asset management will now come with a corridor approach where one entity will own a sizeable segment of a continuous road and maintain it. The funds from monestisation will be utilised for development of other stretches. There will be a lower concessionaire risk because the toll would already have been stabilised and there would be a fair forecast of the revenue model. This is a long-term investment opportunity since the concessions are going to be for about 30 years or so. Within two-three years, we will have a reliable toll figure. In the soon-to-be launched Phase I of TOT, we will have those projects that have already seen at least five years of tollable operations so that traffic estimates are very reliable and the real intrinsic value of the “current-day cost” (net present value) can be assessed.

As of now, 10 projects have been shortlisted for the first round of bidding; six of these are located in Andhra Pradesh and four in Gujarat. Authority obligations are being met – there are no issues in that. If there is a variation in toll collection in the first 10 years (plus or minus 20 per cent), then the authority will compensate by increasing the concession period. If there is an increase in the toll collection, we will decrease it by only half of what would have been given to the concessionaire. In case of any admitted change in law because of which the financial model changes, the authority will enforce the same conditions that prevailed before the change in law. To be considered as a qualified bidder, the entity either itself or through its operations and maintenance (O&M) partner, should have expended at least 40 per cent of the total estimated O&M costs of the project bundle as O&M costs over the past five years and handled a certain minimum number of road projects (each of which spans at least 5 per cent of the total length of the project bundle) as an O&M contractor. The financial criteria will be based on the net worth of the bidder.

TOT is a good investment opportunity. Concessionaires will have to provide the best O&M services. With this, operational efficiencies are expected to increase. For investors, there is no construction risk. They will have an operational road with stable cash flows. I think TOT will be one model which will satisfy the need of higher returns for global pension funds and deep pocketed investors and will have a reliable and very low-risk matrix.

The way ahead

The current scenario for the road sector is bright. Broadly speaking, our government is very committed to infrastructure development. It already has a roadmap and we are probably going to at least double the road length that we have already constructed. So, there is lot of scope which I see for at least the next seven to 10 years.