A merger of the existing 11 government-owned oil companies was proposed by the Ministry of Finance in Union Budget 2017-18. In the budget speech, the ministry proposed the creation of an integrated public sector oil major which will be able to match the performance of international and domestic private sector oil and gas companies. The government has set a disinvestment target of Rs 725 billion for the financial year 2017-18 through stake sales in oil and gas public sector undertakings (PSUs).

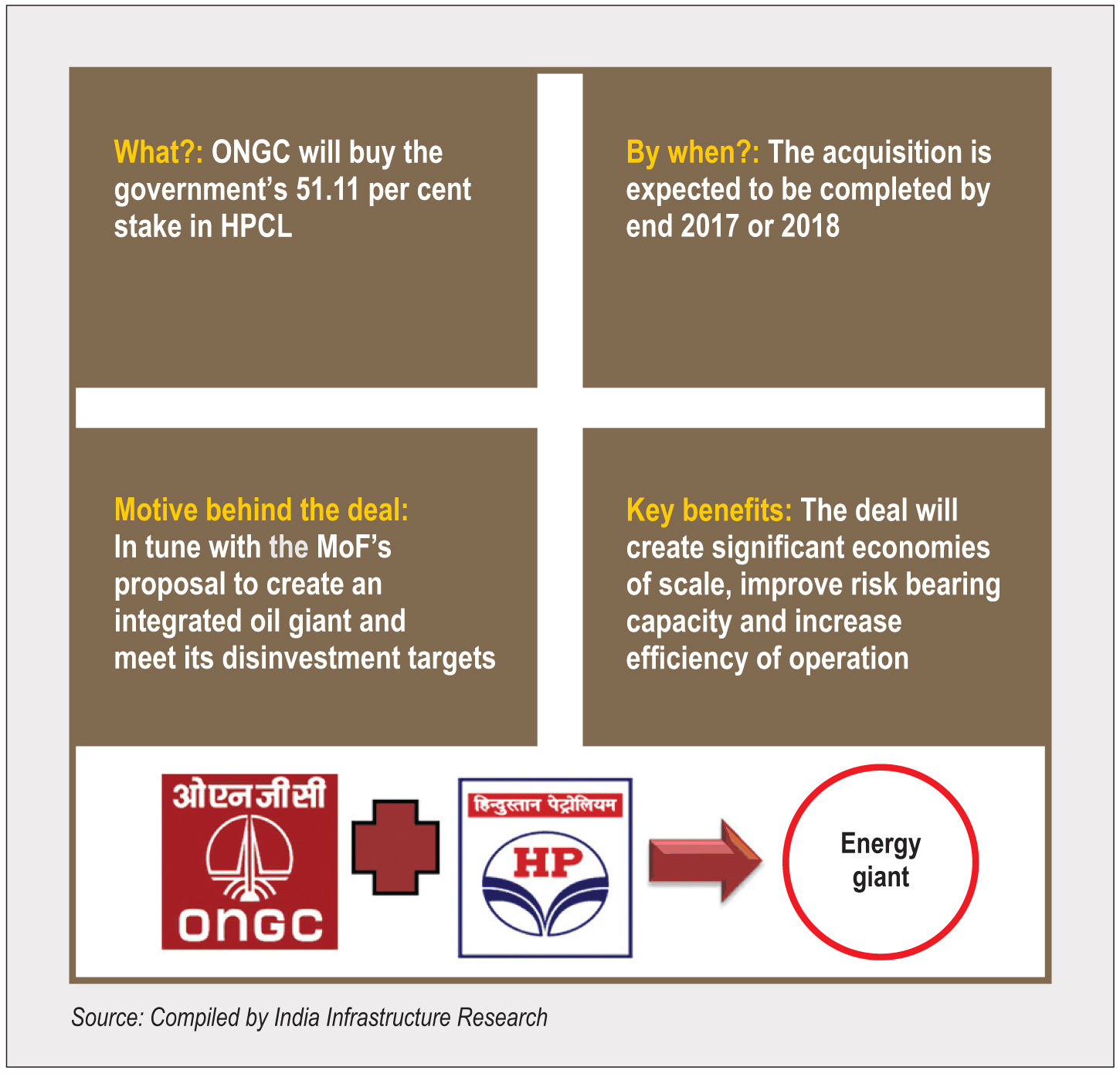

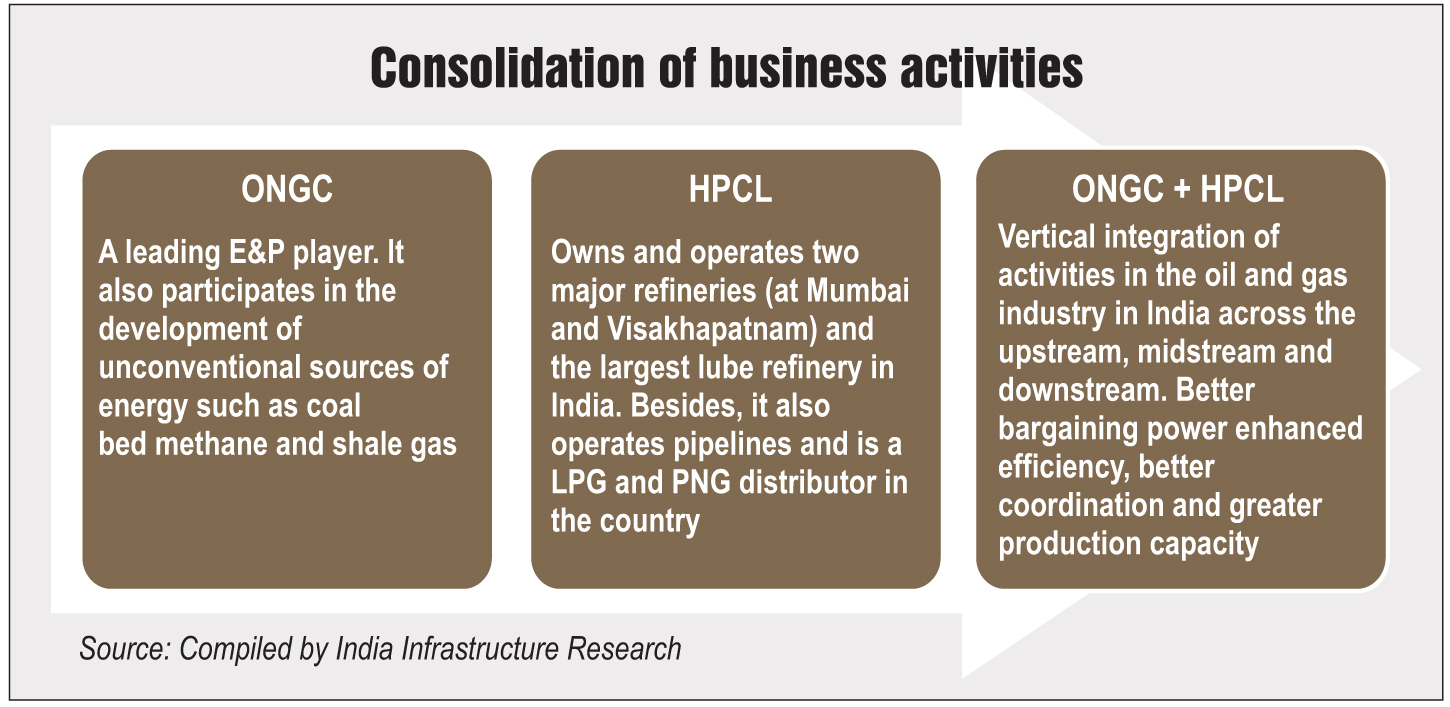

Subsequent to the announcement, the Oil and Natural Gas Corporation (ONGC), one of India’s largest crude oil and natural gas exploration and production (E&P) companies, evaluated options of acquiring either Hindustan Petroleum Corporation Limited (HPCL) or Bharat Petroleum Corporation Limited (BPCL) — two of the major oil refining and fuel marketing companies in the country. Though acquiring either one of the companies made business sense, after undertaking financial analysis, ONGC realised that BPCL was too expensive to acquire and hence decided to acquire HPCL. With this, plans have been set in motion for the creation of an oil giant. The ONGC-HPCL deal, which is expected to materialise by end 2017, will help the government meet at least 40 per cent of its disinvestment target, without losing control over HPCL.

Nitty-gritties of the deal

According to the proposal, ONGC will purchase the 51.11 per cent stake owned by the government in HPCL. The deal is expected to be valued at Rs 260 billion-Rs 300 billion. The proposal was approved by the Cabinet Committee on Economic Affairs in mid-July 2017.

Once the acquisition is complete, HPCL will become a subsidiary of ONGC and will remain a listed company. As per industry sources, ONGC will not have to make an open offer to HPCL’s minority shareholders as the government’s stake is being transferred to another state-run firm and the ownership is not being changed.

Prior to the merger, HPCL is likely to take over Mangalore Refinery and Petrochemicals Limited (MRPL) to bring all ONGC’s refining assets under one unit. HPCL will acquire MRPL either by buying out ONGC’s shares or through a share-swap, wherein ONGC will get more shares in HPCL in lieu of giving up its control in MRPL. ONGC currently owns 71.63 per cent of MRPL while HPCL has a 16.96 per cent stake in the refinery.

Raising resources for the deal

HPCL has a market capitalisation of about Rs 585 billion and buying the government’s entire 51.11 per cent stake will require an outgo of about Rs 300 billion.

ONGC is considering various options to raise funds for the acquisition. It plans to use a mix of internal resources and debt to fund the deal. At present, the company has a cash reserve of about Rs 130 billion. One option that ONGC is considering is raising debt of Rs 250 billion from its shareholders. This will be the company’s maiden borrowing in more than a decade.

Further, the company is also evaluating the option of acquiring the stake through a bulk or block deal at the prevailing market price. The government’s transaction advisor JM Financial and legal consultant Cyril Amarchand Mangaldas are preparing the information memorandum (IM) for the same. The company has appointed SBI Caps and the Citi Group as its merchant bankers for the deal and Shardul Amarchand Mangaldas as the legal advisor, and they will study the IM to arrive at a valuation for the takeover. Besides, other options such as bank loans and the issue of domestic or overseas bonds are also being considered for the purpose of raising funds for the acquisition.

Ripple effects of the deal

- Strengthening ONGC’s balance sheet: The formation of a larger company resulting from the merger of HPCL (a refining company) and ONGC (an upstream oil explorer and producer), will lead to better resistance to volatility in global oil markets. ONGC’s bargaining power will also likely receive a boost post the acquisition. Besides, consolidation across different operations will give ONGC control over the value chain thus leading to strengthening of its balance sheets.

- Improving refining margins: It is expected that HPCL will add 23.8 million tonnes (mt) of annual oil refining capacity to ONGC’s portfolio, thus making it the third-largest refiner in the country after Indian Oil Corporation Limited (IOCL) and Reliance Industries Limited. In the current market conditions, where gross refining margins and marketing margins of refiners are up, the consolidation makes a lot of economic sense.

- A win-win solution: The government will earn about Rs 300 billion as a result of this acquisition. On the one hand, the acquisition will help the government in meeting its disinvestment target, on the other, the transfer of stake from one government-owned company to another will help the government in raising funds without losing control over the two entities. Further, the government’s intent to merge state-run oil companies into a single entity will actually result in the creation of a few large entities with a diversified portfolio – exploration and production, refining, city gas distribution and oil marketing.

- Other key benefits: The acquisition is expected to bring in significant economies of scale, higher risk-bearing capacity, improved margins and increased efficiency.

The way forward

The merger and consolidation of state-owned companies is the only way to meet the centre’s objective of creating an oil giant. The HPCL-ONGC deal is the first step in this direction. It is likely to pave the way for further sector consolidation. In fact, another two deals are in the offing in the oil sector – IOCL’s proposed acquisition of a 66.1 per cent stake in Oil India Limited and BPCL’s acquisition of a 54.9 per cent stake in GAIL (India) Limited. However, these are currently in very preliminary stages of discussion and no further update on the deals is available.

That said, ONGC’s acquisition of HPCL holds significant potential for revolutionising the sector. The resulting synergies will help ONGC get a strong hold over its value chain vertically as well as horizontally and will help it participate and compete in a far more competent manner across the globe, thus, helping the government meet its target of creating an energy behemoth in the country that is capable of competing globally.