The road sector has gone through a phase of course correction with the evolution of a wide variety of implementation models. These models and their variants were introduced to cope with the financial and structural changes faced by the sector. That said, the recently launched toll-operate-transfer (TOT) model fits well in the current scenario. It will serve the twin needs of efficient operations and maintenance (O&M) of existing assets as well as generate funds to be used for ongoing and upcoming highway development projects. The features and significance of various implementation models and the potential for asset monetisation in the road sector are highlighted in the article.

The development and improvement of national highways is a constant challenge for the authorities and requires innovation at every step. One of the critical aspects of the large-scale development of modern highways is the availability of funding options, which requires financial engineering in the creation and management of road assets.

The authorities certainly have a huge task on their hands, given the size of the Indian road network which spans a length of 5.5 million km. The network handles about 60 per cent of the total freight and 90 per cent of the passenger traffic in the country. The involvement of multiple organisations for the management of the network makes the task even more challenging. The extent of congestion on national highways can be gauged by the fact that less than 2 per cent of the total Indian road network carries about 40 per cent of the road traffic. Thus, management of the network is critical to ensure growth of the economy.

India is one of the few countries to have involved the private sector in owning and operating highways under the public-private partnership (PPP) model. This is despite the fact that in India there is no specific law to protect the interests of the private investor. Globally, this has been considered a prerequisite for any successful PPP programme. Another important point is that in India, PPP as a concept was accepted while the financial framework for funding PPPs was still at a nascent stage. Overall, the experience of PPPs in the road sector can be considered good, with a few exceptions of failures or super success.

This can be attributed to the concept of “adaptability to innovation”. When we say innovation, it need not to be from the global perspective but from an Indian perspective. The Indian road sector has been innovative in the development and implementation of various models. In any scheme of things, the user is the most important and critical stakeholder. That said, users agreeing to adapt to the concept of “pay per use” is reflected in their willingness to pay for better road facilities. The success of PPPs depends on an appropriate risk-reward allocation with a focus on “partnership”, a key aspect. The point here is that PPPs should be treated not as another form of contracting, but as a partnership with good faith in each other’s ability. The degree of adaptability of the concept of equal partners will determine the success of the framework. In addition to “monetary” capital, the biggest contribution of the private sector should be “efficiency” capital.

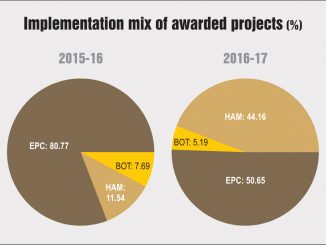

The PPP structure has evolved based on past learnings and opportunities. It started as toll- and annuity-based concessions depending on the viability of the project. Later, the structure evolved to toll plus annuity and very recently to hybrid annuity, which is a combination of the engineering, procurement and construction (EPC) and annuity models. While these models are applicable to the development of road projects, the O&M of road sections developed by the National Highways Authority of India (NHAI) or other road authorities continues to be a daunting task. However, various formats have been adopted to ensure the efficient O&M of roads. One significant format was operate, maintain and transfer (OMT). The OMT model, though, could not produce the desired results and this is attributable to issues related to the contract period, project bankability and the scientific assessment of the project corridor.

Apart from O&M, raising funds for the ambitious expansion and upgradation of national highways is the need of the hour. The popular adage “necessity is the mother of innovation”, also holds true here. Challenges being faced by the highway authorities have led to the conceptualisation of the TOT model. On the one hand, the TOT model ensures the O&M of the project and, on the other, it allows the monetisation of the future cash flow potential of a project stretch.

The TOT model gives the right to collect toll to the concessionaire for pre-selected road packages with an obligation to maintain the road package during the concession period. In lieu of this right, the concessionaire has to pay an upfront fee to NHAI. Under the TOT structure, the role of each equity/fund provider and the concessionaire with O&M capabilities has been clearly defined. During the entire journey of PPP projects, the role of a developer and that of a contractor was not clearly delineated. In certain cases the stressed balance sheets were a result of some contractors trying to act as developers and developers trying to simultaneously wear two hats – that of the developer and an EPC player.

As concession periods under the TOT model are in the range of 25-30 years (and may go up further by about 20 per cent), investors need to have a long-term horizon for returns on investment. The concessionaire also needs to have the capacity to sail through any down cycle during this long tenure. This gives tremendous opportunity to a new set of investors. These long-term players are in the class of sovereign, insurance and pension funds looking for sturdy, long-term investment opportunities. Meanwhile, as a part of the TOT team, O&M players can focus on operations with a long-term perspective and adopt new technologies in the areas of O&M as well as tolling. Creating the right space for the right players will certainly lead to clarity among stakeholders and will create a platform for them to collaborate while leveraging their individual strengths.

A critical examination of the model reveals that the TOT structure needs a few modifications to ensure that it meets the expectations of the risk assessment teams of the large fund houses. Risk dimensions should be looked at differently vis-à-vis traditional contractors/developers. The commitment of all stakeholders to be partners will be key to the model’s success.

In the TOT structure, the concept of a “data room” to provide good diligence to a prospective bidder is certainly a step in the right direction. However, it could have been better had NHAI vouched for the correctness of the data. In the absence of this, this data can only act as a point of reference, and not a point of assurance, which is again highly desirable for the success of this model.

The model in general warrants that bidders take a call on various macroeconomic dimensions. However, they certainly have no control and no tool available to them to make any predictions on the same. These macroeconomic variables depend on complex factors such as local and international factors on one the side and political decisions on the other.

GDP growth, inflation rates and interest rates are a few indicators and the TOT model requires bidders to take a call on them. While the model has some inbuilt incentives, these are not sufficient to mitigate the nature and the size of the risk. These issues have been discussed in the earlier versions of PPPs as well, but somehow they have made an unwelcome comeback. This might force bidders to take a more conservative approach while bidding and NHAI may miss out on capturing greater value.

A few rounds of consultations may be required to tweak the model and eliminate its shortcomings. Nonetheless, the TOT model is the need of the hour. It is certainly a bold step by the authority to develop a modern, forward-looking tool which is a win-win for all stakeholders. The TOT model, if implemented in the right form and spirit, has the capacity to change the face of the road sector in India forever and for the better.

Praveen Sethia, Founder and Director, Infrastructure Advisors Private Limited

Praveen Sethia, Founder and Director, Infrastructure Advisors Private Limited