The construction equipment industry went through a torrid time between 2012 and 2015, during which growth plummeted. It was only last year that the revival process began and sales started getting back to 2011 levels. Since then, the construction equipment sector has been hit by a series of headwinds, with the most recent being the goods and services tax (GST) that came into effect in July 2017. However, the long-term outlook seems to be bullish owing to the government’s intent of removing all implementation bottlenecks, the recent fiscal stimulus package to the road sector, demand for technologically superior equipment from the coal sector to meet the 1 billion production target, and big-ticket government programmes and schemes.

Equipment sales

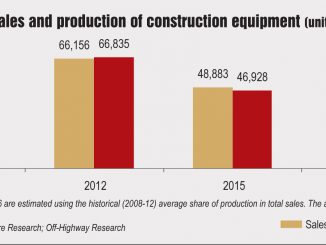

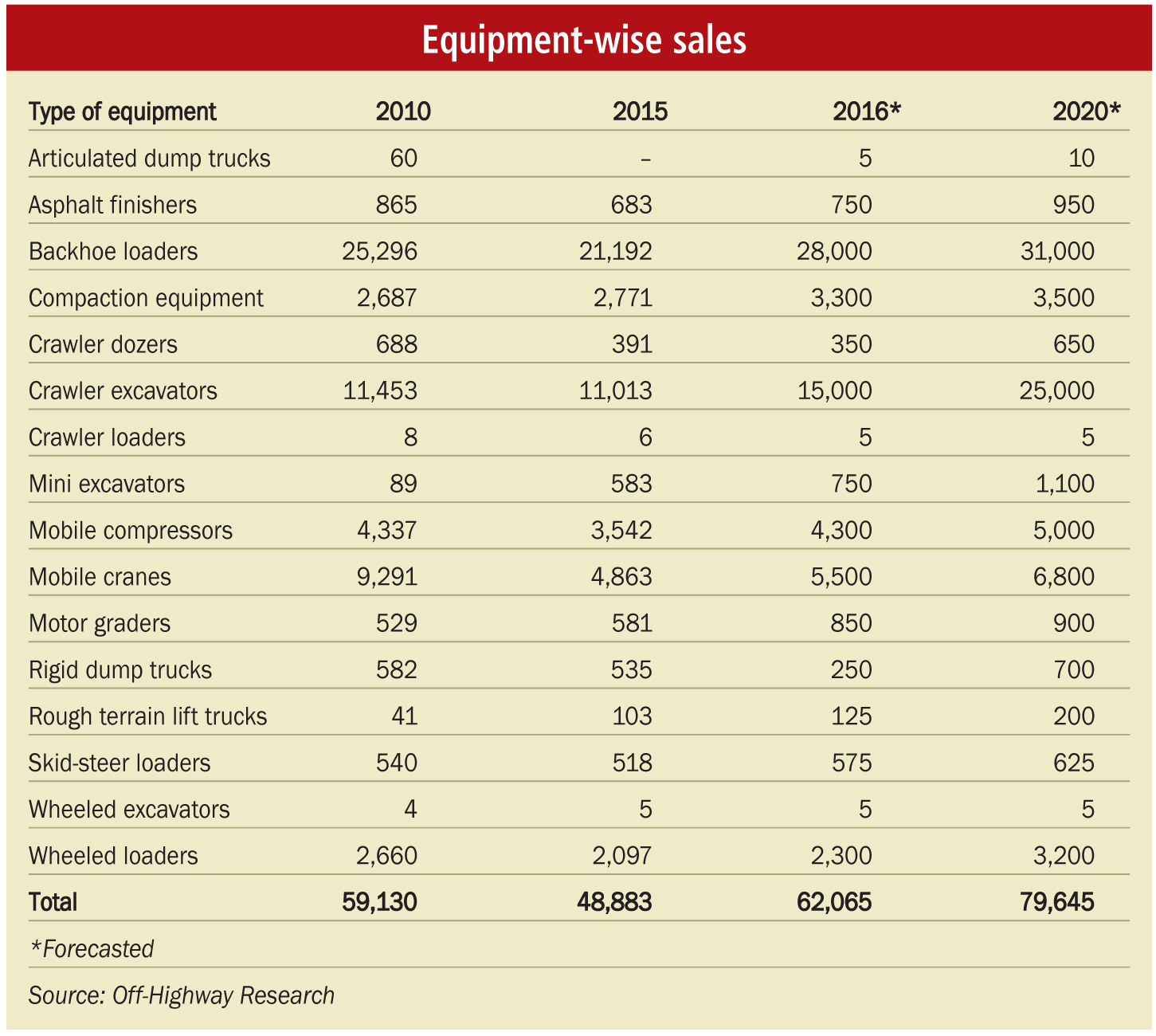

The period 2012-14 has been marked by a declining trend in terms of sales of construction equipment in the country. According to Off-Highway Research, the market declined by 8 per cent in 2012, 16 per cent in 2013, and 14 per cent in 2014 to a low of 47,889 units. However, in 2015, the declining trend reversed, and the market grew by 2 per cent to 48,883 units. Estimated sales of construction equipment increased by 27 per cent to 62,065 units during 2016. The recovery in 2016 is understood to have been driven by the road sector, translating into higher sales of equipment such as backhoe loaders, crawler excavators, motor graders and mobile compressors rising.

Technological upgradation

India, in its second phase of mechanisation in the construction equipment segment, is witnessing a shift in demand from basic equipment to more advanced technology, as users have to deal with tighter project schedules, greater accountability in meeting quality parameters, and a need to ensure greater safety. In recent years, there has been tremendous modernisation in construction equipment, with most original equipment manufacturers (OEMs) launching technologically advanced and energy-efficient equipment at regular intervals. Their objective is to enhance productivity, reduce downtime, bring in cost competitiveness, reduce reliance on imports, and manage a better inventory of spares.

An interesting outcome of this trend is that small and medium contractors are rapidly becoming main contractors. They are bidding for projects and are going in for the latest equipment in order to meet their project timelines, and also because the more technologically advanced equipment has less wear and tear, and lower operating costs and downtime.

Another notable trend is the integration of automation and intelligent systems with equipment. Periodic and predictive maintenance alerts not only help in minimising downtime and operational costs, but also enable the owner to keep an eye on the machine through a smartphone. The owner is alerted as to the machine’s location, in case of any unauthorised use, or theft of fuel or machine part, which is quite common at project sites.

Rental and leasing market

According to industry sources, the rental and leasing equipment market in India is pegged at $2 billion. Around 20 per cent of equipment used annually is hired. Most of the transactions take place locally through brokers in an opaque manner and the unorganised segment caters to nearly 70 per cent of the rental and used equipment volumes. With the easy availability of financing schemes and the increasing use of construction equipment, the scope of the construction equipment rental industry is growing.

iQuippo: In October 2016, Srei Infrastructure Finance Limited launched India’s first online marketplace for leased and rental construction equipment. The platform is the first digital marketplace for construction equipment, machinery and services. It allows construction equipment owners to list their assets/services, negotiate with buyers, finalise terms of a deal, generate digital contracts/invoices, and receive real-time payments. The platform will offer total solutions for all types of construction and mining equipment and will also provide value-added services like asset certification, valuation, parking, maintenance, logistics, spare parts and manpower.

Ground realities

For the first time in five years, in 2016, the earth-moving and construction equipment industry grew after the much required push from the government in terms of budget allocations and resuming stalled projects, especially in the road sector. This has pushed capacity utilisation to 50-70 per cent from around 40 per cent in 2010-11. However, in December 2016 the industry was hit by the demonetisation, though for a brief period. Then in April-May this year sales were hit badly due to the confusion about the court order on the ban on BS-III automobiles.

Subsequently, the GST, enforced on July 1, 2017, has also had an impact on the construction industry. According to the Indian Construction Equipment Manufactures’ Association (ICEMA), 80 per cent of construction equipment machinery has been put under the 28 per cent tax slab while the remaining will be taxed at 18 per cent. Most of the vehicles that contribute to the overall sales of construction equipment in the country such as backhoe loaders and excavators will now be taxed at 28 per cent. These are vital for raising the rate of road building to 40 km per day by March 2018 from the current 23 km a day. Besides, the railway sector, including metro rail, is also picking up. The earthmoving and construction equipment industry plays a significant role in the Swachh Bharat Mission, in which the bulk handling of solid waste is possible only with these machines.

Another factor that is worrisome for the industry is that under the GST regime imported construction equipment, the majority of which comes from China, will become cheaper and this will hurt the domestic industry in the long run. This is because the government has allowed taking tax credit on imported construction equipment, which was not the case earlier, thereby leading to a reduction in the landed cost.

All these factors combined will have an effect on the cash flow of contractors who cater to the infrastructure sector. Therefore, the ICEMA has cut the growth forecast for the construction equipment industry to 5 per cent from the earlier estimate of 15-20 per cent for the ongoing financial year.

Outlook and the way forward

Government initiatives such as Make in India and Skill India, as well as the recent policy push in the form of the National Capital Goods Policy, 2016, bode well for the construction equipment industry. With the government’s announcement of a Rs 7 trillion package for the road sector and the overall increase in infrastructure spend, the demand for construction equipment will accelerate in the coming years. Although the general elections scheduled in 2019 are expected to cause a slight blip in the reviving demand, the prospects continue to remain bright in the long term.

The outlook for equipment manufacturers and providers is optimistic, on the back of a robust pipeline of infrastructure projects. Equipment manufacturers need to streamline their products, integrate new technologies, and upskill their after-sales service and maintenance teams. In fact, the way forward for them is to become total solutions providers rather than just equipment sellers. They can also leverage knowledge sharing and hands-on training for their high-end equipment in order to bring in higher levels of productivity and efficiency.

From the construction equipment industry’s point of view, the only sector that grew last year was roads and highways. The railway sector has shown some progress, though it still needs to “break free” for significant growth. In the irrigation sector too, it is now becoming increasingly clear that the country just cannot continue to depend on monsoons, and measures will have to be taken to develop irrigation infrastructure. Infrastructure sectors as a whole have to exhibit better performance so as to ensure sustainable growth in the construction equipment segment.