")

Merger and acquisition (M&A) activity in India touched a six-year high in 2016, more than doubling to over $60 billion, as compared to around $30 billion in 2015. This included acquisitions by corporates, private equity deals and asset sales. Some big-ticket deals played a crucial role in driving the total value of M&A deals to a record level. These were especially prominent in the oil and gas space, followed by other sectors such as pharmaceuticals, financial services and infrastructure. Factors such as debt restructuring, asset sales and easing credit conditions steered domestic consolidation, which continued to dominate the M&A landscape. Cross-border deal activity also saw an increase despite global headwinds. While inbound activity was driven by relaxed foreign direct investment norms and a stable macroeconomic environment in the country, the momentum in outbound deals was on account of domestic companies expanding their global footprint.

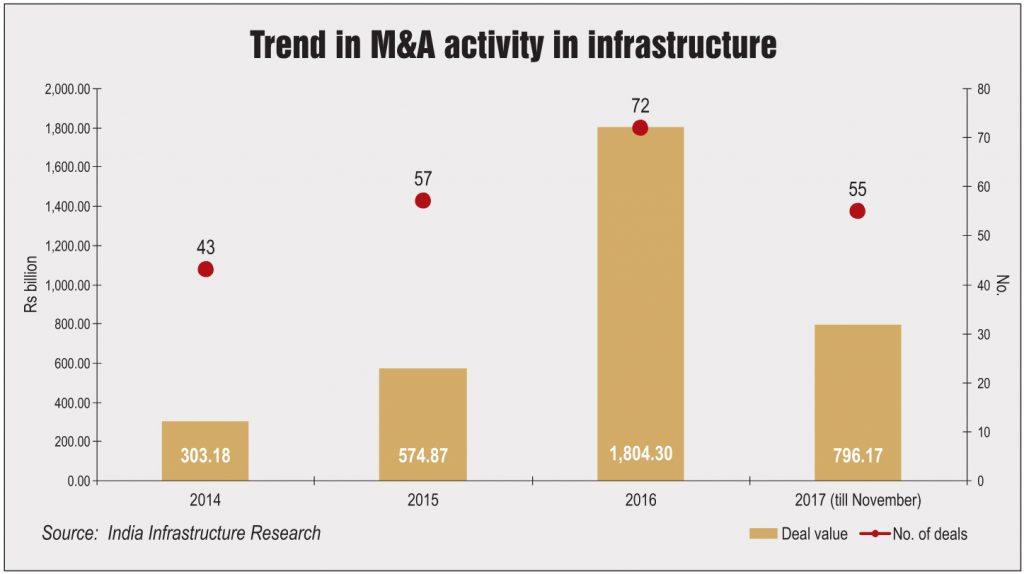

M&A trend

Between 2014 and 2017, the M&A environment was robust on account of companies tapping the inorganic route to either consolidate market share or offload assets to pare debt. Further, interest from financial investors (including private equity (PE) players, pension funds and sovereign wealth funds) has been high, particularly in well-managed, stable cash flow-generating assets, which contributed to the increasing trend.

Sector-wise, oil and gas has witnessed significant M&A developments over the past few years. As the balance sheets of several oil and gas companies have taken a severe hit due to falling crude oil prices, these players are therefore looking at asset monetisation as a means to reduce their unsustainable debt obligations. Another sector witnessing abundant M&A activity is telecom, driven mostly by the pressing need to reduce debt and to obtain higher market shares via consolidation. However, more recently, two major deals in the sector – the Reliance Communications (RCOM)-Aircel merger and the RCOM-Brookfield deal – were called off owing to regulatory uncertainties.

The value and volume of deals, which peaked in 2016, dropped in 2017 on account of diminishing GDP growth mainly caused by demonetisation and the introduction of the goods and services tax. Many investors and businesses adopted a wait-and-watch approach in pursuing big-ticket acquisitions, the primary reason behind lower-value transactions taking place for most part of the year, barring a few big deals. Some of the key ones that were struck in 2017 are the Rosneft-Essar Oil, Cairn-Vedanta, Tata Power Renewable Energy-Welspun Renewable Energy and Hindustan Petroleum Corporation Limited-Oil and Natural Gas Corporation Limited deals.

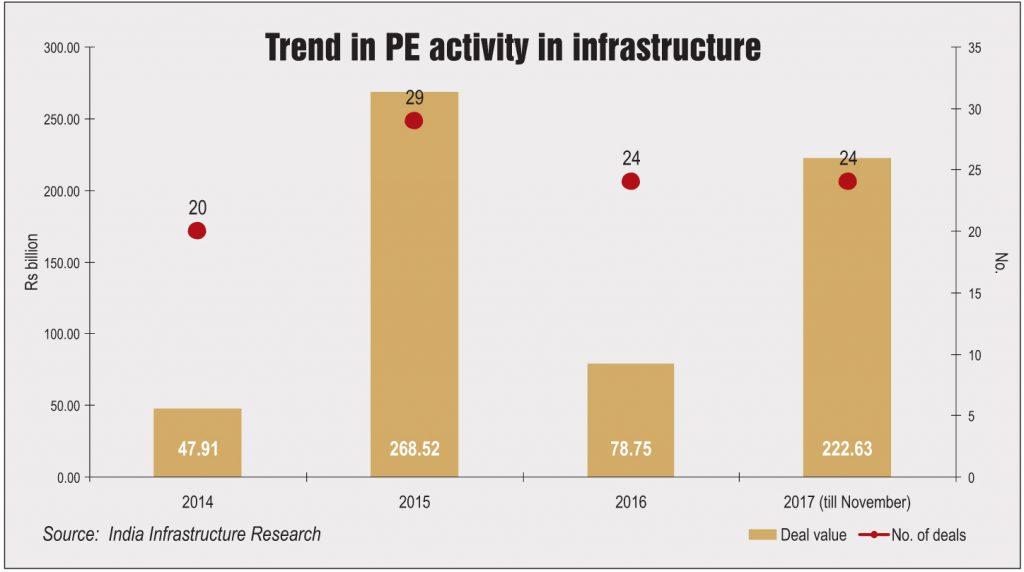

PE trend

PE financing (including private equity in unlisted firms [PEUC], private investment in public equity [PIPE] and project equity [ProE]) has been an important source of funds for infrastructure in India. Between 2014 and 2017, PE activity picked up and reached the highest level during 2015, driven mostly by an uptick in PEUC. The revival was aided by economic growth (resilient to global headwinds), hopes pinned on the new government, new policy announcements, stabilisation of the rupee, and limited options in other emerging economies that mirrored the global economic slowdown.

A sector-wise analysis shows that the renewable energy sector showed heightened PE activity. With new policies and a promising outlook, the sector emerged as the most favoured by investors. This was followed by the telecom and road sectors. The largest PE deal was Centerbridge Partners acquiring Suzlon Energy’s German subsidiary Senvion SE for approximately Rs 75.6 billion. Another key deal during the period was KKR and the Canada Pension Plan Investment Board (CPPIB) purchasing a 10.3 per cent stake in Bharti Infratel for around Rs 61.94 billion.

Since 2015, the infrastructure sector has witnessed a major surge in asset acquisitions. While some companies are offloading assets to deleverage their balance sheets, others are doing so to shift their business focus in a bid to increase market share. The acquisitions have been most prominent in sectors such as real estate, oil and gas, power and roads, where a large number of players are looking to deleverage. In the road sector in particular, a number of companies have exited the build-operate-transfer (BOT) space by monetising operational BOT projects, in a bid to shift the focus back to the engineering, procurement and construction space. Investors are approaching such assets either through direct acquisitions or through purchasing stakes in asset reconstruction companies. In addition, new investment platforms and joint ventures are being formed, specifically targeted at taking exposures in stressed assets. CDPQ-Edelweiss, Piramal Enterprises-Bain Capital and Kotak Mahindra-CPPIB are a few examples of such tie-ups.

PE exits

After experiencing a significant exit overhang till 2013, PE investors have finally exited a number of past investments since then. During 2016, a total of 14 PE exits took place, slightly less than those witnessed in the preceding year. Most of these were partial exits and gave moderate to fair returns to the investors. Most of the transactions were through strategic sales and the secondary market. In 2017, the trend lost steam, and only six exits were seen till November. With regard to returns, there was a mixed trend – some investors took a haircut while others reaped fair returns.

The way forward

As per industry reports, M&A activity is expected to remain vibrant and increase threefold by 2019. The government’s pro-business policy stance has helped establish the right environment for growth. This, coupled with the focus on fiscal discipline, controlling inflation and improving the corporate tax regime and regulatory environment, has set the stage for a sustained growth trajectory for the Indian economy. In addition, as one of the biggest importers of oil, the country has benefited significantly from low oil prices in the international market.

Of all the types of PE investments, PIPE is the option that is the least preferred by PE players at present. In the past, PIPE investments in infrastructure have returned both positive and negative figures, due to which PE firms are bearish on the segment. Sectors such as logistics, which is largely unorganised and offers significant potential for growth capital, are in focus. With regard to PEUC, PE investors appear bullish on the space in the medium term. PE firms are hopeful of a robust array of opportunities in the form of fresh projects in sectors such as renewable energy and logistics.

The overall outlook for asset sales in the infrastructure sector is extremely optimistic. Industry experts believe that the trend has just set in, and is only going to move northwards in the near to medium term. A fundamental reason for this is the fact that the indebtedness of companies is reaching unsustainable levels. Simultaneously, the crackdown of the central bank on non-performing loans is only getting stricter. These factors together are forcing the companies to monetise their assets to stay afloat.

Sector-specific dynamics will also have an important bearing on deal activity. In roads, for instance, nine toll-operate-transfer projects have been identified for near-term roll-out and thus will form a lucrative opportunity. In conventional power, stressed assets (the status of 34 stressed assets has been recently reviewed by the government) may be put on the block in the near future. In the renewable energy space, market consolidation is expected to continue (especially in the solar segment), which may translate into a surge in asset sales. While company-to-company asset acquisition is likely to continue in sectors where players are looking to expand through the inorganic route and gain a greater foothold in the market, interest from PE players is also encouraging, owing to their growing preference for acquisition of operational projects.