")

After a period of slow growth, the Indian meter market is now witnessing a shift in demand and technology. It is upbeat about the revival of demand backed by various government schemes such as the Ujwal Discom Assurance Yojana (UDAY), the Integrated Power Development Scheme (IPDS) and the Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY). Metering technology is also constantly evolving to cater to the increasing demand for advanced metering solutions that focus on energy management in addition to the traditional accounting, monitoring, and billing functionalities. The government also plans to install 30 million smart meters by 2019 to enable two-way communication between the utility and the consumer. Further, utilities are laying greater emphasis on metering as it helps in identifying high-loss pockets. Remedial measures can be taken towards the reduction of aggregate technical and commercial (AT&C) losses.

An overview of the Indian metering market, government schemes driving metering uptake, and utility and meter manufacturers’ perspective…

Market overview

The size of the metering market is estimated at Rs 30 billion with organised players accounting for over 80 per cent of the total size. The market size is expected to increase over the next few years given the government’s targets for smart meter deployment and AT&C loss reduction.

As per the Indian Electrical and Electronics Manufacturers’ Association, the growth index of meters recorded a -1 per cent growth during April-June 2017 and -13.9 per cent growth during 2016-17 due to delays in the implementation of various government schemes.

Public and private power distribution utilities are the largest consumers of meters in the country. The other consumer groups include industrial and commercial establishments, whose requirement varies from panel meters to smart meters. Meanwhile, for power utilities, the highest demand is for residential and grid meters. Currently, electronic meters are dominating the market owing to the high replacement rate of old electromechanical meters. It is estimated that still over 20 per cent of the meters are electromechanical or static.

Metering initiatives under government schemes

Various government schemes like 24×7 Power for All, UDAY, the IPDS, the DDUGJY and the National Smart Grid Mission (NSGM) encourage the installation of smart meters and enable feeder metering.

UDAY mandates operational performance improvement for discoms through smart metering and metering of urban and rural feeders. Under the scheme, progress on rural and urban feeder metering has been quite impressive with 100 per cent achievement across 24 states. However, progress in distribution transformer (DT) metering has been unsatisfactory so far as only about 56 per cent of the targeted 1.5 million urban transformers and 46 per cent of the targeted 4.2 million rural transformers were metered as of November 2017.

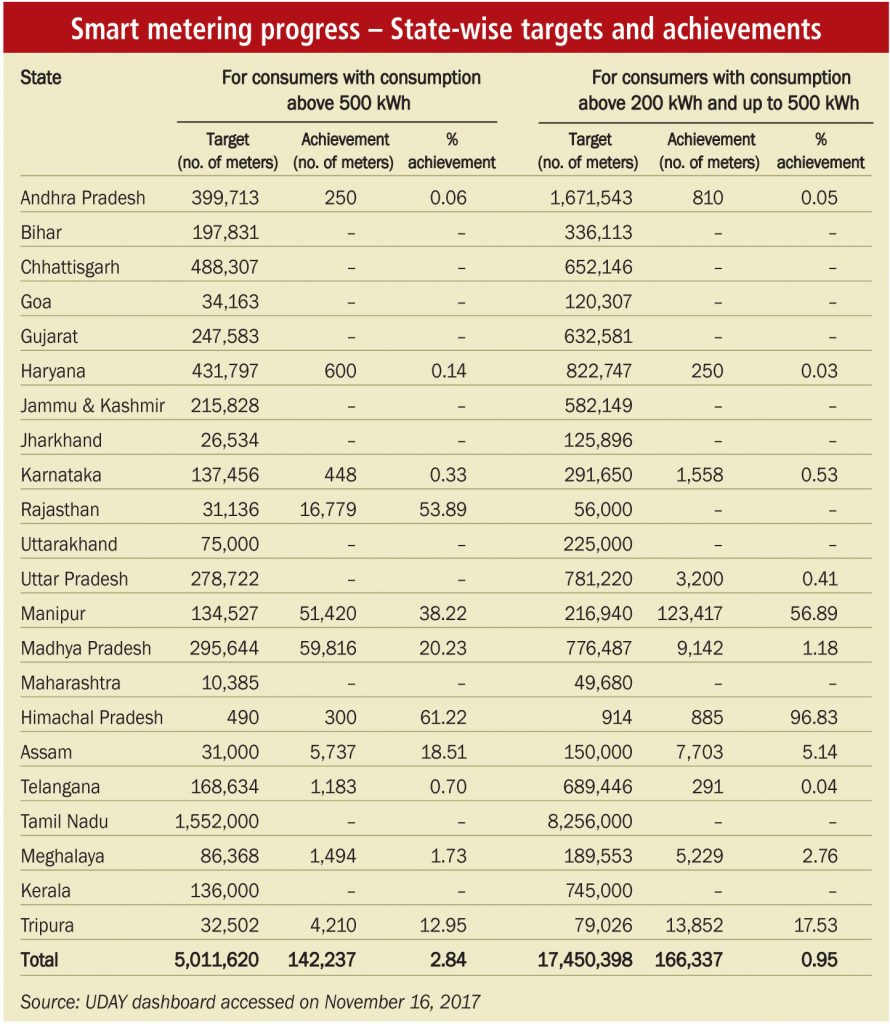

Moreover, as per the MoUs signed by states, smart meters have to be installed for consumers with a consumption of more than 500 units per month by December 31, 2017, and for those with a consumption of over 200 units per month by December 31, 2019. However, the progress on this front has been tardy mainly due to the high cost of smart meters. As of November 2017, only 3 per cent of the targeted 5 million consumers (above 500 kWh) and barely 1 per cent of the targeted 17.5 million consumers (200-500 kWh) were covered.

Metering is a vital component of the IPDS as well. Under the scheme, utilities are expected to make provisions for installing meters at all levels – DTs, feeders and consumers – in the urban areas. The total amount sanctioned for system strengthening (including metering) under the scheme is Rs 161.5 billion, of which Rs 42.8 billion (about 26 per cent) has been released so far. In addition, in October 2017, the Ministry of Power (MoP) approved the balance outlay of Rs 7.5 billion under the IPDS for implementing smart metering solutions in well-performing UDAY states. Meanwhile, under the DDUGJY, which focuses on metering in rural areas, projects worth Rs 38.6 billion have been sanctioned so far.

Under the NSGM, four smart grid projects are under way, one each at Chandigarh, Amravati, Congress Nagar (both in Maharashtra), and Kanpur (Uttar Pradesh). In addition, 12 pilot projects, partially funded by the MoP, are being implemented at various locations across the country. These projects primarily focus on functionalities such as advanced metering infrastructure, distribution transformer monitoring, substation automation, peak load management, outage management and demand response.

Utility issues

Distribution utilities across states have taken steps to increase metering coverage over the years. As per India Infrastructure Research, over 95 per cent consumers in the domestic, commercial and industrial consumer categories were metered as of 2015-16.

However, metering agricultural consumers is a challenge for utilities owing to the high cost of meter procurement, remote location of irrigation pump sets and farmers’ resistance. At present, the cost of a single-phase meter is about Rs 500 while that of a three-phase meter is Rs 1,200-

Rs 1,400. With the launch of the Saubhagya scheme, the utility’s metering requirement for rural consumers is expected to increase further. If unmetered connections are provided under Saubhagya, consumers may use power indiscreetly, leading to an increase in AT&C losses.

Further, with regard to the government’s mandate to install smart meters, the utilities are facing challenges due to the high cost of smart meters (about Rs 5,000 per meter). Therefore, to reduce the cost of smart meters they are taking steps such as the issuance of bulk tenders for meter procurement. One such tender was recently released by Energy Efficiency Services Limited (EESL) for the procurement of 5 million smart meters, wherein the lowest bid of Rs 2,503 per single-phase smart meter (by ITI Limited) was achieved. This is about 50 per cent less than the prevailing market price of smart meters.

Among other issues, the interoperability of meters with various devices and equipment presents a challenge for utilities. Further, there is a lack of adequate testing facilities, which leads to delays in meter installation.

Manufacturers’ concerns

A significant portion of meter manufacturers’ revenue comes from state power discoms and any delay in payment has an adverse effect on their financial position. Therefore, the discoms’ ability to pay is crucial for meter manufacturers and suppliers. In the case of smart meters, there is a lot of deliberation taking place in the industry with regard to the cost of meters and the return on investment for manufacturers. Another key challenge for the industry is the adoption of an appropriate funding model for the development of metering technologies, as to whether it should be a 100 per cent capex model, a 100 per cent opex model or a mix of both.

In addition, meter manufacturers need to prevent any tampering with the meter as well as the data. Further, meter specifications are not well defined by utilities. This impacts the meter development process.

Going forward, the power sector needs end-to-end metering, which is vital for proper energy accounting, billing, load forecasting and planning of network augmentation/expansion. The deployment of radio frequency (RF)-based meter technology in urban pockets and infrared technology in rural areas is also expected to in-

crease. Meanwhile, the requirement of smart meters over the next few years is estimated at 30 million. In addition, the demand for net metering solutions is expected to increase with the government’s target of 40 GW of rooftop solar power by 2022. Prepaid meters are also witnessing increasing uptake as they help reduce the percentage of under-recovered revenue. Further, the government is planning to install prepaid meters under the Saubhagya scheme.

In terms of states, the demand for meters in Maharashtra is estimated at 1-1.5 million meters in the next two years, while in Andhra Pradesh and Punjab, it would be in the range of 300,000-600,000 meters. Punjab is focusing on implementing RF in a big way and a pilot project is under way in Mohali. Meanwhile, 4 million smart meters will be installed in Uttar Pradesh and 1 million in Haryana over a period of three years.

Overall, the metering industry seems bullish about its future prospects in terms of demand, though certain issues pertaining to the high cost of meters and meter specifications need to be addressed jointly by utilities and meter manufacturers. Going forward, metering will play a crucial role in facilitating sustainable commercial operations of distribution utilities.