")

India’s growth story has been an impressive one, withstanding global headwinds witnessed in recent times. Though there has been some deceleration in the past year, the country’s performance is still better than that of many of its counterparts. As per the provisional estimates of national income released by the Central Statistics Office, the growth rate of GDP at constant market prices was 7.1 per cent in 2016-17 as compared to 8 per cent in 2015-16. Although recent moves, including the note ban and the introduction of the goods and services tax, caused a dent in GDP growth in the current fiscal year, the economy has shown early signs of improvement in the second quarter of 2017-18.

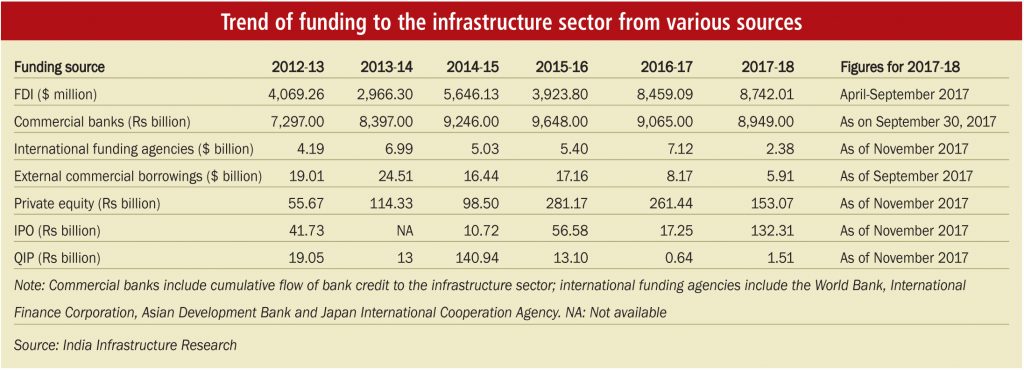

Infrastructure financing in the country has been a vexed issue. The crucial role played by commercial banks in the past in lending to the infrastructure sector has led to a huge pile-up of non-performing assets (NPAs) and has constrained this source of funding. As a result, alternative funding mechanisms are desperately needed. Meanwhile, the initial public offering (IPO) market for infrastructure has made a comeback in the current fiscal year, after losing steam in 2016-17.

Considering various sources of infrastructure funds, bank credit constitutes the largest share. As of September 2017, the banking sector’s exposure to the infrastructure space was over Rs 8.95 trillion, a decline over the Rs 9.06 trillion reported at the close of 2016-17. Considering the sector-wise exposure, the maximum share was cornered by two sectors – power and roads – as was the case in the previous fiscal year as well. As of September 2017, around 78 per cent of the cumulative exposure pertained to these two sectors. The grim lending scenario was mainly an outcome of the cautious approach adopted by lenders, given the rising NPAs and the large number of debt restructuring cases.

During 2017-18 (till September 2017), external commercial borrowings (ECBs) and foreign currency convertible bonds (FCCBs) worth $5.91 billion were tapped into by infrastructure companies. The total amount raised during the period under consideration was 55 per cent higher than the previous year’s corresponding figure of $3.8 billion. During the year 2016-17, fundraising through ECBs and FCCBs amounted to $8.17 billion. ECBs have become a less-tapped route in the past 15-20 months. The slowdown in private investment has been cited as one of the reasons for the declining trend. In addition, falling domestic interest rates vis-à-vis global interest rates have left little incentive for domestic companies to borrow from the overseas market.

Lending by international agencies during the year was not very significant. In 2017-18 (till November), the World Bank committed $731 million towards three projects, while the Asian Development Bank (ADB) extended financial assistance to the tune of $1,275 million to three projects. In 2016-17, the World Bank had approved loans worth $1,455 million towards five projects and ADB approved loans to the tune of $3,193 million towards nine projects.

On the equity front, the scenario was far better. During 2017-18 (till November), 18 private equity (PE) deals worth Rs 153 billion have been witnessed, an improvement from the 16 deals worth Rs 55.42 billion that were witnessed during the corresponding period of 2016-17. In the entire fiscal year 2016-17, 27 deals worth Rs 261.44 billion were recorded. Renewable energy attracted the maximum number of deals. During 2017-18 (till November), five PE exits were witnessed. Of these, three were in the renewable energy space, and one exit each in telecom and diversified segments. During the corresponding period of 2016-17, 12 exits were reported in the infrastructure space.

Activity in the capital market also was noteworthy. A number of players in the infrastructure sector issued IPOs to raise equity. In 2017-18 (till November), 10 companies raised funds to the tune of Rs 59.48 billion through public floats. The biggest issuance – Rs 14.42 billion – was by Cochin Shipyard Limited. During the year 2016-17, four firms raised a total of about Rs 17.25 billion through the IPO route.

Meanwhile, infrastructure investment trusts (InvITs) have finally seen the light of day. The ongoing fiscal year witnessed public issuances of two InvITs – the IRB InvIT Fund and India Grid Trust – worth a total of Rs 72.83 billion. Despite strong investor response, the issues made a weak stock market debut.

As far as equity inflow through the foreign direct investment (FDI) route is concerned, the quantum surged in 2017-18 (till September). During the period, infrastructure sectors attracted $8.74 billion through the route, higher than the $8.46 billion worth of FDI equity inflow during the year 2016-17. Sectors such as telecom and air transport were responsible for the increasing trend. The eased FDI norms in construction, aviation, railways, etc. have boosted investor confidence and the government’s Make in India initiative has further attracted foreign funds to the country.

Meanwhile, bond issues are finally picking up. Over the past 15-18 months, a higher offtake for bonds was reflected by higher volumes. The majority of this was witnessed in the form of private placements through private companies. Companies such as Delhi International Airport Limited, Reliance Jio Infocomm Limited, Adani Ports and Special Economic Zone Limited and Great Eastern Shipping Company Limited tapped the bond market to raise funds. Among investors, life insurance companies, foreign institutional investors and mutual funds subscribed to the issues. Besides, green bonds are also gaining traction gradually. Companies such as ReNew Power Ventures, the Greenko Group, IDBI Bank, Axis Bank and NTPC Limited have raised large sums through green bonds.

There were some developments with regard to new funding sources, including the National Investment and Infrastructure Fund. The fund closed its first major deal worth $1 billion with the Abu Dhabi Investment Authority. Meanwhile, the New Development Bank and the Asian Infrastructure Investment Bank have also extended credit to various infrastructure projects in the past 12-15 months.

Pension and insurance funds continue to contribute far less than their potential. However, many foreign sovereign wealth funds, pension funds and PE players are placing bets on stressed assets in the country, particularly in the power and roads space. Several cash-strapped promoters are putting their operational assets on the block to deleverage their balance sheets. Meanwhile, the launch of schemes such as the Strategic Debt Restructuring Scheme and the Scheme for Sustainable Structuring of Stressed Assets have been instrumental in expanding the market for asset sales. Though these have had only limited success so far, the crackdown on unpaid dues has proved sufficient to persuade troubled companies to monetise their assets and pare outstanding dues. The interest of investors in such operational/near-completion projects is being driven by the scope of turning them around and selling them at a profit at a later stage.

In sum

With the country reaping the benefits of a conducive business environment and the government’s initiatives to facilitate investment, the short- to medium-term outlook of the infrastructure sector appears buoyant. There is significant progress in the roll-out of new infrastructure projects in the country, a sizeable part of which will be supported by direct government funding. The recent Rs 7 trillion package for the road sector is evidence of this. Renewable energy projects will continue to be the key driver of credit growth in the infrastructure sector in the next one-two years. On the policy front, the introduction of enabling regulations, greater clarity on policy matters and the stability of a long-term infrastructure policy have become imperative to further bolster investor confidence. Besides, in order to enhance private participation, it is important to implement projects in a timely manner and find innovative and optimal ways to manage the financing of these investments.